The moments after you spot roof damage—a sudden leak dripping onto your floor or shingles scattered across the lawn—are absolutely critical. What you do right then and there sets the stage for the entire roofing insurance claims process.

Taking the right steps from the get-go is your best defense against a complicated or denied claim, and it’s what will get your home back to normal as smoothly as possible.

What to Do When You First Find Roof Damage

It’s natural to feel a wave of panic, but a methodical approach will serve you much better. Before you even think about picking up the phone to call your insurance company, your top priorities are safety and documentation.

Safely Assess and Document the Damage

First things first: never climb onto a roof you suspect is compromised. It’s just not safe. The good news is you can gather a ton of powerful evidence right from the ground with just your smartphone.

Take a slow walk around your property. Photograph and video everything that looks out of place. Be thorough.

Get specific with what you’re looking for, as different storms leave different calling cards:

- Hail Damage: Look for obvious circular dents or subtle "bruises" on your shingles. Don't forget to check gutters, downspouts, and roof vents, too.

- Wind Damage: Scan for shingles that are missing entirely. Also, look closely for any that are lifted, curled, or have a visible crease down the middle where the wind bent them back. The edges and ridges of the roof are always the most vulnerable spots.

- Debris Impact: Make a note of any tree limbs or other objects that have landed on your roof.

Your initial photos are invaluable. If your phone can timestamp them, even better. Capture wide shots showing the entire slope of the roof, then zoom in on the specific points of damage you found. This early evidence is gold.

Mitigate Further Damage Immediately

Your insurance policy actually requires you to take reasonable steps to prevent the problem from getting worse. In the industry, this is known as damage mitigation.

If you have an active leak, this is as simple as placing buckets to catch the water. It shows you’re being responsible.

Key Takeaway: For a significant hole or breach in the roof, getting the area covered with a tarp is a non-negotiable step. This single action demonstrates to your insurance provider that you are proactively protecting your property, which is a condition in almost every policy. Make sure you keep the receipts for any tarps or materials you buy for these temporary fixes—they are often reimbursable.

Review Your Insurance Policy First

Okay, before you make that call, find your homeowner's insurance policy. This document is the rulebook for your claim.

You'll want to find the section on wind, hail, or storm damage to get a clear picture of your specific coverage. Pay close attention to your deductible—that's the amount you have to pay out-of-pocket before your insurance kicks in.

Knowing this number upfront is crucial. It helps you decide if filing a claim even makes financial sense, especially for more minor damage. Nailing these first few actions lays a solid foundation for a successful claim.

Building an Undeniable Roof Damage Claim

After a storm, it's tempting to just snap a few quick photos and assume you’ve done your part. But I’ve seen time and again how that approach falls short. To build a claim that gets approved without a fight, you need to provide a comprehensive evidence package that leaves no room for doubt.

Think of yourself as building a case file. The more organized and detailed you are, the smoother the entire roofing insurance claims process will be. This is more critical now than ever, as insurance carriers are tightening their requirements and demanding more thorough documentation before they’ll approve a claim. You’re not just a homeowner anymore; you're a prepared claimant.

Create a Detailed Damage Log

Your first move should be to start a simple but consistent log. This document becomes your single source of truth, a running record of everything that happens from day one. It doesn't need to be fancy—a notebook or a note on your phone works just fine.

For every piece of damage you spot, make an entry with a few key details:

- The Date of the Storm: Pinpoint the exact date the damage happened. You can easily cross-reference this with local weather reports.

- Observed Damage: List every single issue you notice. Be specific. It's not just "shingles missing," it's "5 shingles missing from the southwest slope." Note the dented gutters, too.

- Photo References: Make a note of which photos correspond to which item of damage. For example, "Photos DSC_0012-DSC_0015 show the dented flashing."

This organized approach immediately tells the adjuster you're serious and meticulous. It builds instant credibility. And if the storm caused any interior damage to your belongings, you can strengthen your claim even more by creating a comprehensive home inventory.

Master the Art of Evidentiary Photos

The photos you take are the absolute backbone of your claim. An adjuster who might be hundreds of miles away needs to see the full story of the damage, from the big picture all the way down to the smallest detail.

Your photo collection should tell a complete story. Make sure you capture:

- Wide-Angle Views: Take photos of all four slopes of your roof. This gives the adjuster context and shows the roof's overall condition before you zoom in on the problems.

- Close-Up Shots: Now, get in close. For hail damage, put a coin or a tape measure next to a dent to show its size. For wind damage, get a picture of the crease on that lifted shingle. These details matter.

- Collateral Damage: This is the one most homeowners forget. Document damage to the surrounding property. Take pictures of dented AC units, torn window screens, chipped siding, or dinged-up gutters. This collateral evidence helps prove the storm's intensity and validates your roof damage claim.

Pro Tip: Before you start snapping pictures, turn on the timestamp feature on your phone's camera. Dated photos provide indisputable proof of when you documented the damage, directly connecting it to a specific storm and shutting down any potential arguments about pre-existing conditions.

Your Essential Roof Claim Documentation Checklist

Use this checklist to gather every piece of evidence you need to build a powerful and effective insurance claim.

| Documentation Type | Why It Matters | Expert Tip |

|---|---|---|

| Damage Log | Creates a clear, chronological record of all damage and communications. | Update it immediately after every phone call or email with your insurer. Note the date, time, and person you spoke with. |

| "Before" Photos | Proves the roof's good condition prior to the storm. | Check your phone's photo gallery or old real estate listings for pictures showing your roof before the damage occurred. |

| "After" Photos | Provides visual evidence of the extent and specific nature of the damage. | Take more photos than you think you need. Capture wide, medium, and close-up shots of every issue. |

| Collateral Damage Photos | Substantiates the storm's intensity and its ability to damage your roof. | Photograph dented gutters, damaged fences, torn window screens, and chipped siding. This is powerful supporting evidence. |

| Repair Estimates | Documents the professional cost of restoring your roof to its pre-storm condition. | Get at least two itemized estimates from reputable, local roofing contractors. Avoid storm chasers. |

| Proof of Ownership | Confirms your legal standing to file a claim on the property. | A copy of your property deed or mortgage statement is usually sufficient. |

| Home Insurance Policy | Outlines your specific coverage, limits, and deductible. | Keep a digital and physical copy. Highlight the sections on roof damage and replacement cost value (RCV) vs. actual cash value (ACV). |

By presenting this well-documented package, you transform from just another claimant into a prepared partner in the process. This level of professionalism not only helps your adjuster do their job more accurately but can also dramatically speed things up.

Choosing the Right Roofing Contractor for Your Claim

After a storm rolls through, your choice of roofing contractor becomes the single most important decision you'll make. This isn't just about finding someone to nail down shingles; you need a skilled advocate in your corner who truly understands the ins and outs of the roofing insurance claims process. This person provides the detailed, accurate damage assessment that becomes the foundation of your entire claim.

Most homeowners know to ask, "Are you licensed and insured?" While that’s absolutely essential, it's just the table stakes. To find a real partner for this process, you need to dig much deeper and ask the questions that separate a true claims specialist from a simple repairman. A great contractor is your ally, first and foremost.

Questions That Reveal a True Claims Expert

When you start interviewing potential contractors, their answers to a few specific, claim-focused questions will tell you everything you need to know. Don't hold back—any reputable roofer who deals with insurance work will welcome this level of scrutiny.

Try asking these direct questions to really gauge their expertise:

- "Can you walk me through your experience working with my specific insurance company?" You're looking for a confident, specific answer. A seasoned pro might even mention adjusters they’ve worked with before.

- "How exactly will you support me when the insurance adjuster comes to inspect my roof?" The only right answer here is that they will be physically present, on the roof with the adjuster, pointing out every detail of the damage and explaining their assessment using industry-standard language.

- "What's your game plan for handling a supplemental claim if the insurance company's initial estimate is too low?" A real professional will have a clear, established process for documenting everything the adjuster missed and negotiating for the funds needed to do the job right.

Their responses will quickly separate the pros from the pretenders. You want someone who sees themselves as part of your team, ready to fight to get all legitimate damage covered.

Red Flags to Watch for When Hiring

Just as important as knowing what to look for is knowing what to run from. The chaos after a major storm can unfortunately attract some less-than-honest players, and recognizing their tactics is your best line of defense.

Be extremely cautious of any contractor who offers to "cover" or "waive" your deductible. It might sound like a great deal, but this is a classic sign of insurance fraud. A roofer willing to deceive an insurance company might not think twice about cutting corners on your roof, like using cheaper materials or unqualified labor.

Keep an eye out for these other major warning signs:

- High-Pressure Sales Tactics: If a contractor is pushing you to sign a contract on the spot, that’s a huge red flag. Take your time.

- Vague or Incomplete Estimates: Always insist on a detailed, itemized quote that clearly breaks down the costs for both labor and all materials.

- Lack of a Local Presence: Be wary of the "storm chasers" who roll in from out of state. They might be long gone when you need them to honor their warranty.

Picking your contractor is the most influential decision you'll make during this whole process. A great local roofer like Paletz Roofing and Inspections doesn't just give you a precise damage assessment—they act as your advocate, making sure the insurance company sees the full, true scope of necessary repairs. This partnership is absolutely essential for getting a fair and complete settlement.

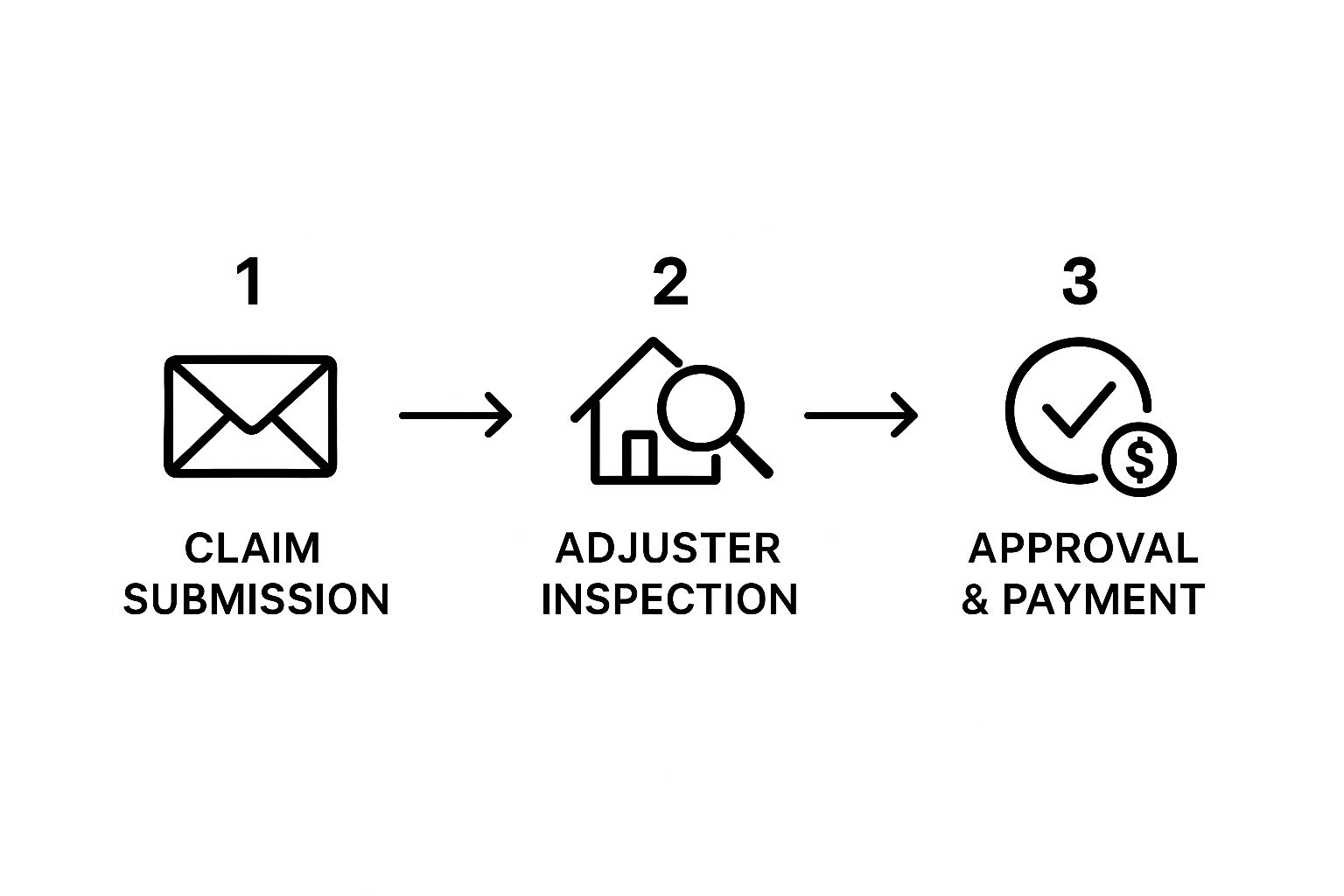

Filing the Claim and Meeting the Adjuster

Alright, this is where the rubber meets the road. You’ve done your homework, documented the damage, and picked a great contractor. Now it's time to officially kick off the roofing insurance claims process. This part involves two big conversations: your first call to the insurance company and the on-site inspection with their adjuster. How you handle these interactions can make or break your claim.

When you dial that number, have your info ready. You'll need your policy number, the date the damage happened, and a simple, factual description of the event. The only goal of this initial call is to get a claim number and find out who your assigned adjuster is. Keep it simple and stick to the facts—don't guess about the cost or the full extent of the damage just yet.

This whole process can feel a bit overwhelming, but it really boils down to a few key stages.

As you can see, it moves from your initial filing to that all-important inspection, and then hopefully, to approval and payment.

The Adjuster Meeting: Your Most Important Conversation

The on-site meeting with the insurance adjuster is, without a doubt, the single most critical moment of your entire claim. The adjuster's job is to see the damage firsthand and write an estimate based on their observations. That report is what determines the insurance company's initial settlement offer, so it’s absolutely vital they see everything.

This is exactly why having your roofer present for this meeting is non-negotiable. Your contractor isn't just a bystander; they're your expert advocate on the ground.

Expert Insight: A seasoned roofer and an insurance adjuster speak the same language. Your contractor can point out subtle but critical damage—things like hairline cracks on shingles from hail, or wind-lifted flashing—that an overworked adjuster, who might be inspecting a dozen homes that day, could easily miss.

Setting the Stage for Success

Your contractor will be up on the roof right alongside the adjuster, comparing notes and making sure their professional assessment of the damage is heard and understood. Think of it as a collaborative effort. This simple step helps prevent disagreements and ensures all the real damage gets documented in that first report, which helps you avoid the headache of filing supplemental claims later.

With the cost of roof repairs in the U.S. soaring to nearly $31 billion a year, getting this first assessment right is more important than ever. Much of that cost is driven by severe weather, which now causes over half of all residential roofing claims. You can read the full research on evolving roofing risks to see how these trends are affecting homeowners just like you.

Your job during this meeting is to be the organized, prepared homeowner. Here’s what you do:

- Share Your Documentation: Have your folder of photos and your damage log ready for the adjuster to look over.

- Ask Good Questions: Ask about their process and when you can expect to see their final report.

- Keep it Collaborative: Treat the adjuster like a partner in solving a problem, not an opponent. A little goodwill goes a long way.

When you combine this professional approach with your contractor's hands-on expertise, you create a powerful team focused on one thing: getting a fair and accurate assessment of the damage to your home.

Decoding Your Insurance Estimate and Getting Paid

Once the adjuster has come and gone, you’ll get an email with your insurance estimate, which is often called a Scope of Loss. Let's be honest, these documents can be a nightmare to read. They're packed with industry jargon and weird calculations that don't make immediate sense.

But this isn't just a piece of paper with a number on it. It’s the detailed breakdown of your entire settlement, and understanding how it works is the only way to make sure you get every penny you need for a proper roof replacement.

Key Terms You Absolutely Must Understand

Your estimate is going to be littered with acronyms. The three you’ll see over and over are RCV, ACV, and Depreciation. If you don’t know what these mean, you won’t understand how you’re getting paid.

-

RCV (Replacement Cost Value): This is the big one. It’s the total amount of money it will cost to replace your roof with brand-new, similar materials at today's prices. This is the number we're working towards.

-

Depreciation: Think of this as the value your old roof lost simply due to age and normal wear and tear. Insurance companies hold this portion of the money back until the job is actually finished.

-

ACV (Actual Cash Value): This is what your old, damaged roof was worth the moment before the storm hit. The insurance company gets this number by subtracting the Depreciation from the RCV (RCV – Depreciation = ACV). Your first check will be for this ACV amount, minus your deductible.

Here’s How It Plays Out: Let's say the total cost to replace your roof (RCV) is $20,000. The insurance company decides that your 10-year-old roof lost $6,000 in value over the years (Depreciation). That makes your ACV $14,000. If you have a $2,000 deductible, your very first check will be for $12,000 ($14,000 ACV – $2,000 Deductible). You'll only get the final $6,000 (the depreciation money) after you've sent them a final invoice proving the new roof is on.

What to Do When the Estimate Seems Low

It is incredibly common for that first insurance estimate to come in lower than your roofer’s quote. Don't panic. This is a normal part of the process.

Adjusters are human, and they often miss small but vital line items—things like the cost of specific types of flashing, code-required underlayment, or pulling the necessary permits. This is where your roofer steps back in to file what’s called a supplemental claim. This isn't an argument or a fight; it's a professional, evidence-backed request for the missing funds.

A good contractor knows exactly how to build this supplement. They'll submit a detailed package that includes:

- Clear photos showing the missed damage or required components.

- An itemized list of costs for the missing materials and labor.

- Direct references to local building codes that mandate these items.

This gives the adjuster the documentation they need to approve the additional funds. With nearly 50% of all homeowners insurance claims in the U.S. being for wind and hail, you can bet that insurance carriers are extremely familiar with this process. You can dig into more storm damage claim trends on sunsent.com.

A roofer who is experienced with insurance claims knows precisely how to handle this negotiation. Their job is to bridge the gap between that initial lowball estimate and the actual cost of doing the work right. This advocacy is one of the most important things a claim-savvy roofer does for you, ensuring your project is fully funded without you having to cut corners.

Answering Your Top Questions About the Claims Process

Even with a perfect game plan, the roofing insurance claim process can still feel a bit murky. It's completely normal for questions to pop up, and frankly, you should be asking them. I've been helping homeowners with this for years, so I've heard just about everything. Here are the answers to the most common—and pressing—concerns that come up along the way.

How Long Does a Roofing Insurance Claim Usually Take?

This is the million-dollar question, and the honest answer is: it depends. A typical claim can wrap up in a few weeks or drag on for several months. The timeline really hinges on a few key variables. If you’ve got your ducks in a row with clear, thorough documentation right from the start, things will move a whole lot faster.

The biggest factor, hands down, is storm volume. If a major hurricane just tore through your area, adjusters are going to be absolutely swamped. You can, and should, expect delays. Your insurance company's own internal process and how responsive they are also plays a huge part in how quickly things move.

Another common hold-up is a supplemental claim. This happens when your roofer inspects the damage and finds that the adjuster's initial estimate is too low or missed critical items needed to do the job right. Your roofer will then submit a supplement for the additional funds. This back-and-forth negotiation can easily add several weeks to the process. Once everyone agrees on the numbers, the first check is usually issued pretty quickly, with the final payment (called the depreciation) released after you show proof that the work is finished.

Here's a real-world example: A client of ours in Miami filed a claim right after a hurricane. Because of the sheer number of claims in the area, it took three weeks just to get an adjuster to their property. The initial estimate was way off, so we filed a supplement. After two more weeks of negotiation, the supplement was finally approved. All told, the time from filing the claim to getting the final payment was just over two months.

What Should I Do If My Roofing Claim Is Denied?

Seeing that denial letter in the mail is a gut punch, I get it. But it is absolutely not the final word. The very first thing you need to do is read that letter carefully and pinpoint the exact reason they gave for the denial. Very often, the insurer will chalk it up to "wear and tear" or "improper maintenance" instead of legitimate storm damage.

Do not just accept this. Your next call should be to your roofing contractor. Share the denial letter with them immediately. A reputable roofer will give you a professional second opinion, and if they disagree with the insurance company's assessment, they can help you gather more specific, targeted evidence to fight back.

Armed with this new proof, you can file a formal appeal with your insurance company. If they deny the appeal, you still have other moves you can make:

- Hire a Public Adjuster: These are licensed professionals who work for you, not the insurance company. Their entire job is to negotiate on your behalf to get you a fair settlement.

- Consult an Attorney: For really complex claims or if you suspect the insurance company is acting in bad faith, an attorney who specializes in insurance claims might be your best bet.

Will Filing a Roof Claim Make My Insurance Go Up?

This is probably the question I hear the most, and the answer is usually no—at least, not directly because of your single claim. Most states have regulations that prevent insurance companies from jacking up your rates for filing one claim for weather-related damage, often called an "Act of God." After all, you didn't cause the hailstorm, so you shouldn't be singled out and punished for it.

However, there’s a really important distinction to understand here. If a catastrophic storm causes massive, widespread damage and huge losses for the insurer across your entire region, they might raise rates for everyone in that area. They do this to offset their costs and re-evaluate the risk of insuring homes in that zone. So while your individual claim wasn't the trigger, your rates could still go up as part of a larger, regional adjustment.

Your premiums are far more likely to spike if you file multiple, unrelated claims in a short time frame. That's what really flags you as a higher risk to an insurer.

Navigating all these complexities is so much easier when you have an experienced partner on your side. The team at Paletz Roofing and Inspections has been helping South Florida homeowners through the claims maze for decades. If you're dealing with roof damage, contact us for a free, no-obligation inspection and expert guidance.