Impact-resistant shingles usually cost 10% to 30% more upfront than standard architectural shingles, with Class 4 materials running about $150 to $250 per roofing square compared with $100 to $150 for standard options, and that often adds $2,000 to $5,000 on a typical 2,000 square foot roof replacement (1866 Stay Dry cost breakdown). In South Florida, that higher buy-in can still make financial sense because Class 4 roofs may qualify for 10% to 25% annual insurance premium reductions when the carrier requires a UL 2218 Class 4 rating (UL 2218 discount requirements).

That price gap changes a lot once you stop looking at shingles as a simple material upgrade and start looking at total ownership cost in a high-wind zone. South Florida roofs take sun, wind, flying debris, and storm season stress that expose the weak points in cheaper systems fast.

Homeowners usually ask the wrong first question. They ask, “What do impact-resistant shingles cost?” The better question is, “What will this roof cost me over time if I stay in this house through multiple storm seasons?” That's where impact-resistant roofing starts to look less like a premium add-on and more like a risk-management decision.

Table of Contents

- Understanding the Value of Impact Resistant Shingles

- Average Cost of Impact Resistant Shingles

- A Complete Roofing Project Cost Breakdown

- Key Factors That Influence Your Final Price

- Calculating Your Return on Investment and Insurance Savings

- How to Choose a Qualified Contractor in South Florida

- Frequently Asked Questions About Impact Resistant Shingles

Understanding the Value of Impact Resistant Shingles

An impact-resistant shingle is built to take a harder hit than a standard asphalt shingle. The value isn't just in surviving hail. In South Florida, it's also about handling debris impact, preserving the roof surface longer, and reducing the chance that one storm turns into a repair cycle.

The construction matters. Class 4 impact-resistant shingles use polymer-modified asphalt, which gives the shingle more flexibility under stress and helps it resist cracking when struck. That's different from a basic architectural shingle that may look similar from the street but won't perform the same way under repeated storm exposure.

What you're really paying for

You're paying for a roof covering designed to hold up better when weather gets violent. According to SquareDash's Class 4 shingle guide, Class 4 shingles are rated to withstand 2-inch (50.8 mm) steel ball impacts. That rating matters because it gives homeowners and insurers a recognized benchmark instead of a vague durability claim.

In a market like Broward, Miami-Dade, or Palm Beach, that benchmark has practical value:

- Storm resilience: Better resistance to impact damage from wind-driven debris.

- Fewer service calls: Less chance that a moderate event turns into scattered repairs.

- Insurance relevance: Carriers often care about the tested rating, not just the marketing label.

- Longer planning horizon: A stronger roof system can make budgeting more predictable.

Practical rule: If you're replacing a roof in South Florida and expect to own the home for years, judge the roof by repair exposure and insurability, not just the initial contract price.

Why South Florida owners should look past the bid total

A low quote can still become the expensive option if the roof ages faster, needs more repairs, or doesn't help with insurance. Homeowners here don't just buy shingles. They buy wind-zone performance, code-compliant installation, and a system that has to keep working after the next major storm warning, not just on installation day.

Average Cost of Impact Resistant Shingles

In South Florida, the upgrade to impact-resistant shingles usually adds a few thousand dollars to a reroof, not tens of thousands. For many homeowners, that is the difference between choosing by invoice price and choosing by total ownership cost over the next 15 to 20 years.

A practical starting point is simple. Impact-resistant shingles generally cost more than standard architectural shingles, and Class 4 products sit at the higher end of the asphalt shingle category. On a typical home, the added material cost often translates into a noticeable but manageable premium in the full contract price. In high-wind areas, that premium can make financial sense if it reduces repair frequency and helps with insurance.

Price ranges that matter most

Roofers may quote by roofing square or by total project price. One roofing square equals 100 square feet, so a 2,000 square foot roof usually starts around 20 squares before waste, ridge, starter, and layout complexity are added.

Here is the pricing difference homeowners usually need to understand first:

| Roof material type | Typical cost range |

|---|---|

| Standard architectural shingles | Lower-cost asphalt shingle option |

| Class 4 impact-resistant shingles | Higher-cost premium asphalt shingle option |

The material gap is real, but it is only one part of the decision. A house in Miami-Dade, Broward, or Palm Beach is exposed to wind-driven debris, repeated storm seasons, and insurance pressure that homeowners in calmer regions do not deal with the same way.

What that means on a typical home

On an average-size reroof, the impact-resistant upgrade often adds enough to matter, but not enough to dismiss automatically. I usually tell homeowners to evaluate that extra spend against two questions. How long will you keep the house? How likely is this roof to need storm-related repair work during that time?

For a short-term owner who plans to sell soon, the lower upfront price of standard architectural shingles may still be the right call. For a long-term owner in South Florida, the math often shifts. One avoided repair cycle, one avoided deductible situation, or a few years of insurance savings can offset a meaningful part of the upgrade cost.

That is why bid comparisons need more than a bottom-line number.

A cheaper quote can still be the more expensive roof to own if it leaves you with a product that takes damage more easily or does little to improve insurability.

Where the premium can pay back

Homeowners here rarely regret paying more for a roof that holds up better after a rough season. They regret paying less for a roof that starts generating repair invoices.

The return usually shows up in three places:

- Fewer post-storm repairs: Better resistance to hail and debris impact can reduce small failures that turn into leak calls.

- Insurance discounts: Some carriers offer credits for qualifying impact-resistant products, though the amount varies and you need to verify it before signing a contract.

- More predictable ownership costs: Paying more upfront can reduce surprise spending later, which matters in a market where roof work is rarely cheap.

Why South Florida pricing has to be judged differently

A homeowner in a mild-weather market can focus more narrowly on installation price. A South Florida homeowner should not. The better question is whether the added upfront cost improves the roof's financial performance over time.

That means looking at impact resistant shingles cost as part of a longer ownership window. If the upgrade helps you avoid repairs, supports better insurance terms, and stays serviceable after the kind of weather we routinely see here, the premium is not just a materials upgrade. It is a risk-control decision.

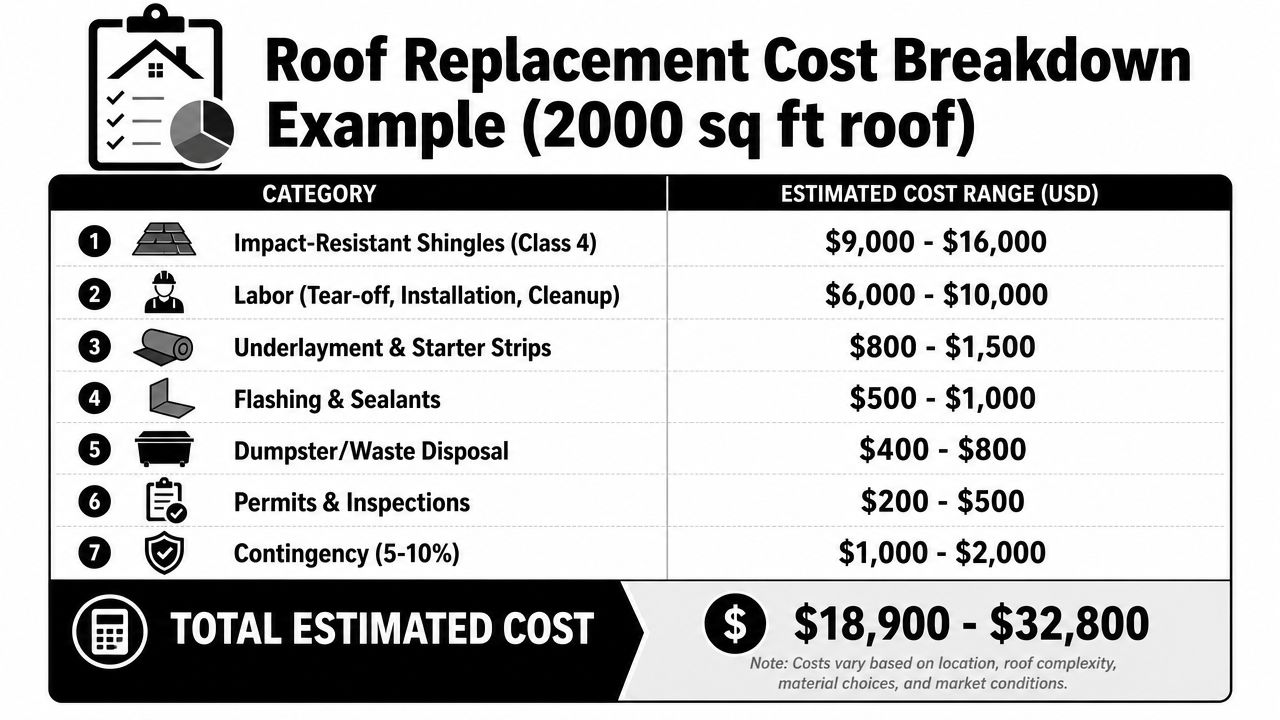

A Complete Roofing Project Cost Breakdown

Homeowners often focus on the shingle price because it's the easiest number to spot. The full roofing quote is broader. A proper replacement includes teardown, deck inspection, underlayment, flashing details, cleanup, permit handling, and labor that matches local code requirements.

If a proposal looks dramatically lower than the others, the missing value is usually somewhere in that system.

What a roofing quote should include

A complete reroof proposal usually accounts for several categories. The exact numbers vary by house and scope, so the right way to review them is by purpose.

- Tear-off and disposal: Removing the old roof and hauling waste offsite. If this line is vague, ask exactly what gets removed.

- Deck inspection and repair allowance: Contractors can't fully assess the deck until shingles come off. If they don't discuss possible damaged decking, the estimate may be incomplete.

- Underlayment and starter materials: These are core water-shedding components. They aren't optional details.

- Flashing and sealants: Valleys, penetrations, walls, and edge transitions are where bad roof jobs usually fail first.

- Shingle installation labor: Skill matters here. A good shingle can underperform if the layout, fastening pattern, or flashing details are wrong.

- Permits and final inspection: In South Florida, permit handling should be clear and documented.

The line items that trigger change orders

The surprise charges usually come from what no one can see before tear-off. Rot, moisture-damaged wood, and failed decking sections don't show up clearly from the ground.

That doesn't mean change orders are dishonest. It means roofing is partly investigative work once demolition starts. What matters is how the contractor explains those items in advance.

A careful homeowner should ask these questions before signing:

- What happens if damaged decking is found?

- How is decking repair priced?

- What flashing components are included in writing?

- Does the estimate include disposal and permit coordination?

- Is cleanup part of the contract or treated separately?

A roofing estimate should read like a scope of work, not like a one-line allowance.

What works and what doesn't in real bids

What works is a proposal that spells out materials, installation scope, and exclusions in plain English. What doesn't work is a low bid packed with broad phrases like “replace roof as needed” or “standard flashing included” without identifying where and how.

In South Florida, the houses that end up with the most expensive reroofs over time are often the ones that started with the cheapest contract, weak details, and too many assumptions. A roof system fails at transitions and penetrations before it fails in the middle field.

When you compare bids, don't just ask, “How much is the roof?” Ask, “What exactly is this contractor replacing, inspecting, and standing behind?” That question will save more money than chasing the lowest number on page one.

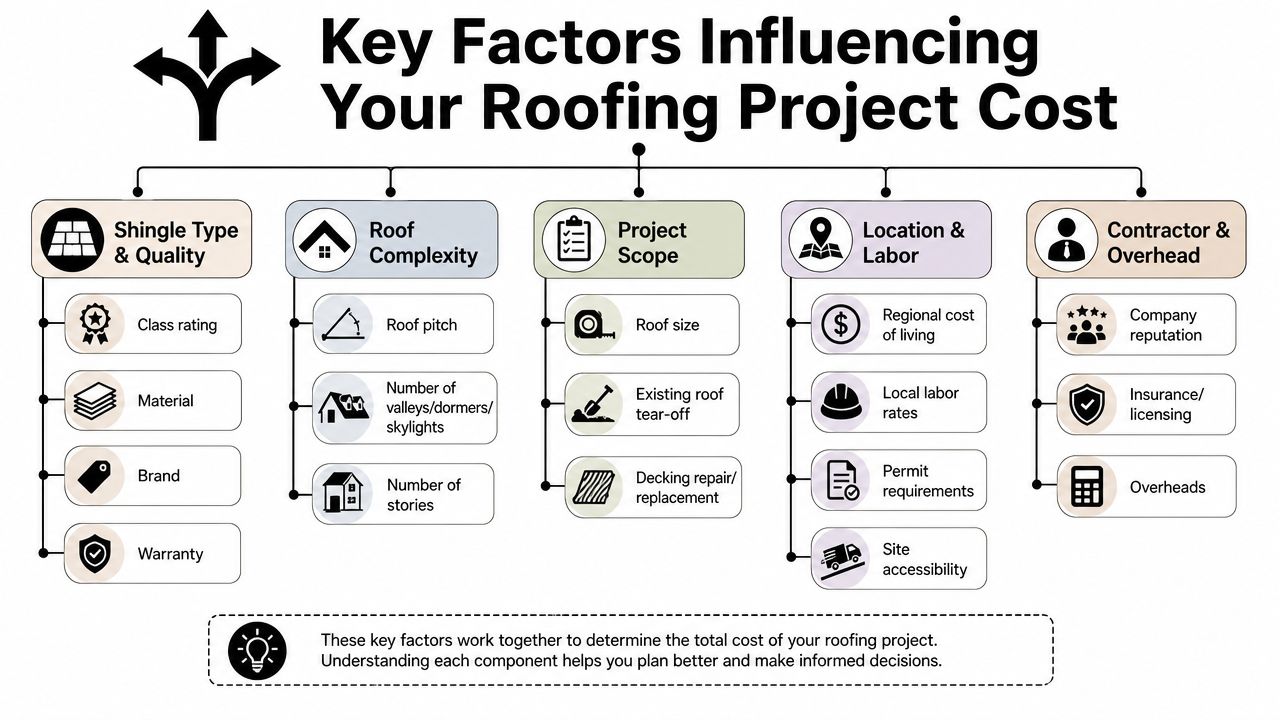

Key Factors That Influence Your Final Price

A South Florida reroof can vary by thousands of dollars even when two homes look similar from the street. The reason is simple. Final price is driven less by the shingle bundle alone and more by roof shape, labor intensity, code-related details, and the long-term cost of owning that roof in a storm zone.

A lower install number can still be the more expensive choice over time if the roof takes more storm damage, triggers more service calls, or misses insurance discounts. In this market, total cost of ownership matters as much as contract price.

Product tier sets the starting point

Impact-resistant shingles cost more because the material itself costs more and the buyer is paying for higher impact performance. Earlier pricing ranges in this article already showed that Class 4 products usually come with a noticeable premium over standard architectural shingles.

That premium is not just about marketing. On South Florida homes, a tougher shingle can reduce the frequency of minor storm-related repairs that add up over the years. It can also improve the roof's value on the insurance side, which changes the overall ownership cost. Homeowners comparing bids should separate two questions: What does this roof cost to install, and what is it likely to cost to own?

Roof design changes labor fast

The same shingle can be affordable on one house and expensive on the next.

A simple, walkable gable roof is faster to tear off, dry in, and shingle. A cut-up roof with hips, valleys, dead zones, skylights, plumbing penetrations, and chimney or wall flashing takes longer at every stage. More cuts mean more waste. More transitions mean more hand work. More detail work means more places where a cheap bid leaves trouble behind.

These house-specific factors usually move the number the most:

- Roof size: More squares raise material, labor, disposal, and delivery costs.

- Pitch: Steeper roofs slow production and increase safety setup.

- Complexity: Valleys, dormers, and penetrations add labor and waste.

- Access: Limited driveway space, pool screens, fencing, and tight lot lines make tear-off and cleanup harder.

- Height: Two-story homes often cost more to stage, load, and protect.

- Existing condition: Layered roofing, soft decking, or deteriorated flashings increase labor and replacement scope.

South Florida code and weather exposure add real cost

South Florida roofs are priced for wind, rain, and inspections, not just curb appeal. Contractors have to account for permit coordination, required fastening patterns, underlayment details, and inspection-ready workmanship. That is one reason bids here can come in higher than homeowners expect.

The weather risk matters too. In a high-wind zone, stronger materials can make more financial sense than they do in calmer parts of the country. A homeowner comparing standard shingles against impact-resistant shingles should also review the insurance side early, not after signing a contract. This homeowner's hurricane insurance guide helps frame how storm exposure affects the full ownership cost.

| South Florida variable | Why it affects price |

|---|---|

| Permit and inspection requirements | More documentation, scheduling, and administrative time |

| High-wind installation details | Fastening and system requirements increase labor and material needs |

| Heavy rain exposure | Better underlayment and flashing details matter more |

| Dense neighborhood logistics | Limited staging and debris handling slow production |

The cheapest line item often creates the highest lifetime cost

I see homeowners focus on the upfront upgrade cost and ignore what happens after the first strong storm season. That is where the wrong roof gets expensive.

If one bid is lower because it uses a standard shingle, lighter system details, or a thinner scope around flashings and accessories, the savings may disappear through earlier repairs, more maintenance, or weaker insurance positioning. If another bid is higher because it includes a true impact-resistant product and cleaner system details, that higher number may produce a better five-year or ten-year result.

How to compare bids without guessing

Ask each contractor to explain three things in plain language:

- What shingle class is being quoted?

- What roof details are included beyond the field shingles?

- What ownership benefits should you realistically expect in South Florida?

A useful quote does more than list a brand and a total. It shows why this roof costs what it costs, and whether the extra money buys lower risk, fewer repairs, or better long-term value.

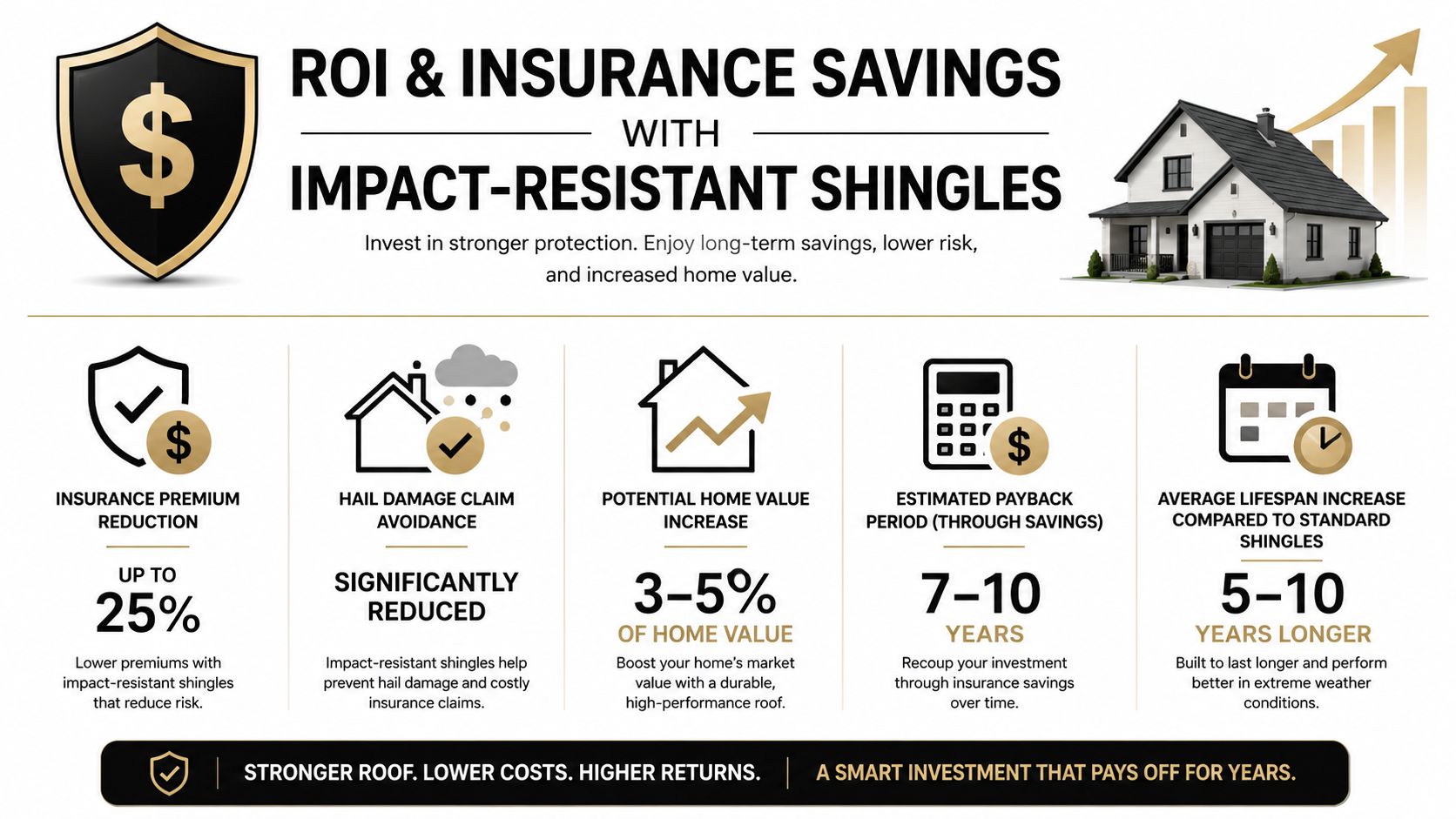

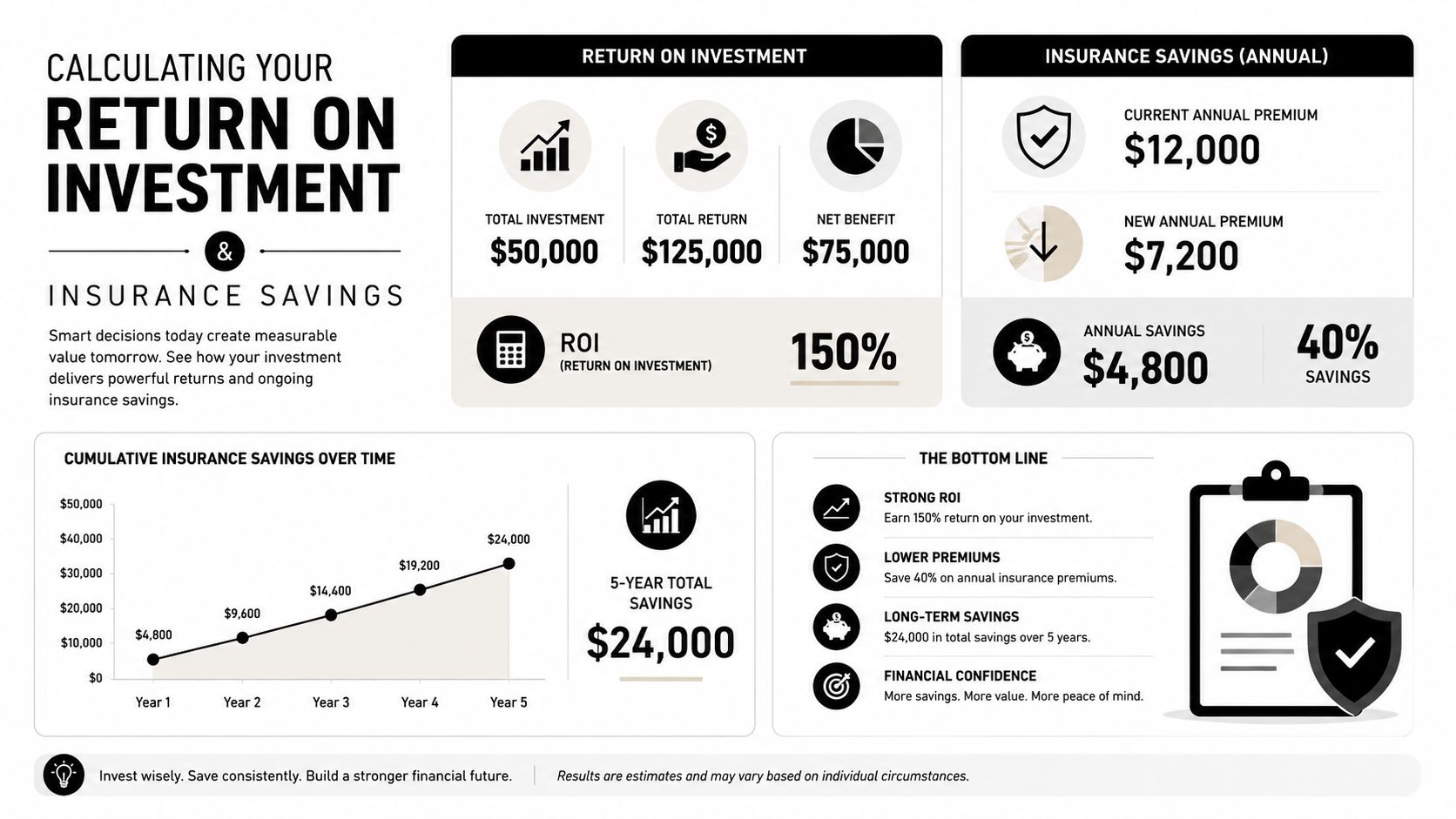

Calculating Your Return on Investment and Insurance Savings

A roof upgrade that adds a few thousand dollars upfront can save money over 10 to 20 years in South Florida. That is the ROI question.

According to Hulsey Roofing's long-term cost analysis, Class 4 impact-resistant shingles typically last 30+ years, compared with 20 to 25 years for standard asphalt shingles, and they reduce 20-year maintenance costs to $500 to $1,500 versus $1,500 to $3,000 for standard shingles. For an owner planning to stay put, those numbers matter more than the line-item upgrade price.

How to calculate the payoff

Use simple math. Start with the upgrade cost for the Class 4 shingle, then compare it against three buckets of savings over time:

- Insurance premium reductions: Some carriers offer discounts for qualifying impact-resistant roofs.

- Fewer repair bills: Small storm hits are less likely to turn into cracked tabs, granule loss, or repeated patch work.

- Longer replacement cycle: If the roof holds up longer, you push a major capital expense further into the future.

Insurance savings are not automatic, and they are not uniform. Carrier rules, wind mitigation requirements, and documentation all affect the result. Before you count on a discount, review your policy and compare it with a solid homeowner's hurricane insurance guide so you understand how roof type can affect premiums, deductibles, and storm claims.

I tell homeowners to run a five-year and ten-year version of the same calculation. If the Class 4 upgrade adds $3,000 to the project, but you recover part of that through lower premiums and avoid even one or two minor storm repair cycles, the gap narrows fast. In a high-wind zone, avoided repairs are a real part of ownership cost.

Why total cost of ownership matters more in South Florida

South Florida roofs take repeated abuse from wind-driven rain, heat, and storm debris. A standard shingle may look cheaper on signing day, but the lower upfront number does not tell you what that roof will cost to own after several storm seasons.

That is why I focus on durability plus paper value. A qualifying impact-resistant roof can help on both fronts if the product is properly documented for the carrier and installed as part of a complete system. Homeowners who keep their records organized, including items like a roof inspection documentation file, are in a better position when they ask for credits or need to support a claim.

{kind=link}

When the upgrade usually pencils out

Class 4 shingles tend to make financial sense under these conditions:

- You expect to stay in the home for several years.

- Your insurer offers a measurable discount for a qualifying roof.

- You are replacing the roof anyway, so the impact-resistant upgrade is an add-on cost, not a separate future project.

- Your property has already had smaller storm-related roof repairs that add up over time.

For South Florida homeowners, the best question is not whether impact-resistant shingles cost more. They do. The better question is whether the extra upfront cost lowers your total ownership cost enough to justify it. In many cases, between insurance savings, fewer repairs, and a longer service life, the answer is yes.

How to Choose a Qualified Contractor in South Florida

A good impact-resistant shingle can still turn into an expensive roof if the installer misses the details. In South Florida, the contractor affects your total cost of ownership almost as much as the product itself. A clean install, correct paperwork, and code-compliant wind detailing are what help you keep insurance credits in place and avoid repair bills after the next storm.

Price matters, but scope matters more. I tell homeowners to compare proposals line by line, because a lower bid often leaves out items that show up later as change orders, failed inspections, or leak repairs around flashing and penetrations.

What to verify before signing

- License and insurance: Ask for current proof, then verify it with the state and carrier.

- South Florida experience: The contractor should know local permitting, inspection steps, and high-wind installation requirements.

- Exact shingle identification: Get the manufacturer name and product line in writing. “Impact resistant” is too vague.

- System scope: Confirm whether the quote includes underlayment, flashing, starter, ridge components, ventilation, disposal, and permit costs.

- Decking policy: Ask how damaged decking is priced if it is found after tear-off.

- Insurance paperwork: Confirm what completion documents you will receive for your records and discount application.

Ask one more question that saves money later. Who handles communication if you have a problem during the job or need documents after completion? Companies that stay organized during storm season usually have better follow-through, and some use tools like Eden AI for roofing professionals to keep calls, scheduling, and customer updates from slipping through the cracks.

What a qualified local roofer should be able to answer clearly

A South Florida contractor should be able to answer these without guessing:

- Which shingle product is being installed?

- What wind-related installation steps are included in the quote?

- What items could increase the final contract price?

- What documents will you receive when the job is complete?

- Who pulls the permit and who meets the inspector?

- If a repair issue comes up later, who is your point of contact?

Vague answers usually lead to vague contracts.

Paletz Roofing and Inspections has been licensed and insured in South Florida since 1990 and works across Broward, Miami-Dade, and Palm Beach counties. Homeowners who want to confirm company identity before scheduling can review the Paletz Roofing and Inspections company logo and inspection file reference.

The right contractor helps the Class 4 upgrade pay off over time. The wrong one can wipe out the savings with paperwork problems, missed details, and repair work you should not have needed in the first place.

Frequently Asked Questions About Impact Resistant Shingles

How can I verify my contractor is installing real Class 4 shingles

Ask for the exact manufacturer product name before installation starts. Then ask the contractor to provide the product documentation and completion paperwork that shows the shingle carries a UL 2218 Class 4 rating. Keep a copy of the proposal, product label information, and final invoice together in case your insurer asks for proof later.

If a contractor only says “impact resistant” without naming the product, that's not enough.

Do impact-resistant shingles come in different colors and styles

Yes. Homeowners usually have multiple style and color choices within impact-resistant product lines. The right approach is to choose the rated product first, then review the available color and profile options that fit your home.

The practical issue isn't whether options exist. It's whether the specific rated shingle you want is available in the look you want.

Are Class 3 shingles ever worth considering to save money

Sometimes, yes. A Class 3 option may make sense when you want some added durability but need to control the initial budget. The trade-off is insurance. As covered earlier, many carriers specifically look for UL 2218 Class 4 if you want meaningful premium reductions.

That makes Class 3 a product decision, not always a financial one.

What helps a roofing company stay organized during storm season

Communication systems matter more than most homeowners realize. During heavy weather periods, missed calls and delayed follow-ups can slow down inspections, estimates, and repair scheduling. Some roofing companies use support tools like Eden AI for roofing professionals to handle inbound calls and keep customer communication moving when field crews are overloaded.

That doesn't replace roofing skill. It just helps the operation stay responsive when demand spikes.

If you want a roof quote that looks at total ownership cost instead of just the lowest upfront number, Paletz Roofing and Inspections can inspect your current roof, explain whether a Class 4 upgrade fits your property, and provide a detailed replacement estimate for your South Florida home.