A wind mitigation inspection is a state-certified review of your home's wind-resistant features that can save Florida homeowners $200 to $1,500 annually on their insurance. It's designed only to provide discounts and cannot increase your premium.

That surprises a lot of new homeowners, especially in Florida, where the wind portion of a policy can be one of the most expensive parts of owning a house. If you're in Broward, Miami-Dade, or Palm Beach County, this inspection isn't just paperwork. It's one of the few home inspections that exists to prove your house deserves insurance credits.

From a roofer's perspective, the value is simple. If your home has the right connectors, roof shape, deck attachment, and opening protection, the carrier wants that documented on the right form. If those features aren't verified, the insurer usually prices the home as if those protections don't exist.

Table of Contents

- What Is a Wind Mitigation Inspection

- Unlocking Major Savings on Your Home Insurance

- The Key Features of a Wind Mitigation Report

- Your Step by Step Inspection Guide

- Sample Findings What Inspectors Photograph

- Schedule Your Inspection with Paletz Today

- Frequently Asked Questions About Wind Mitigation

What Is a Wind Mitigation Inspection

A wind mitigation inspection is a focused inspection that documents how well your house is built to resist wind damage. In Florida, that means the inspector is looking for specific construction details that can qualify your home for insurance discounts, then recording them on the official OIR-B1-1802 form.

This is not the same thing as a code inspection, and it isn't a general safety inspection. The inspector isn't there to tell you whether the whole house is "good" or "bad." The job is narrower than that. The inspection verifies features your insurer uses when deciding whether your home deserves windstorm credits.

Why homeowners should care

If you're new to Florida, consider this: Your roof system is only as strong as the weakest connection in the chain. The roof covering matters, but so do the nails under it, the way the deck is attached, the way the roof is tied to the walls, and whether wind can break openings and pressurize the house from inside.

That's why the inspection matters financially and practically. It gives the carrier proof. Without proof, many homes get priced at the less favorable rate.

Practical rule: A wind mitigation inspection doesn't create protection. It documents protection your home already has, or shows where upgrades may be worth doing.

The broader idea isn't unique to Florida. Good risk decisions always start with documented conditions, whether you're managing a home, a jobsite, or even risk assessments for Australian businesses. The difference here is that Florida insurers tie those documented wind features directly to premium credits.

Homeowners also like the inspection because it turns vague hurricane anxiety into something concrete. You stop guessing. You find out what the home has.

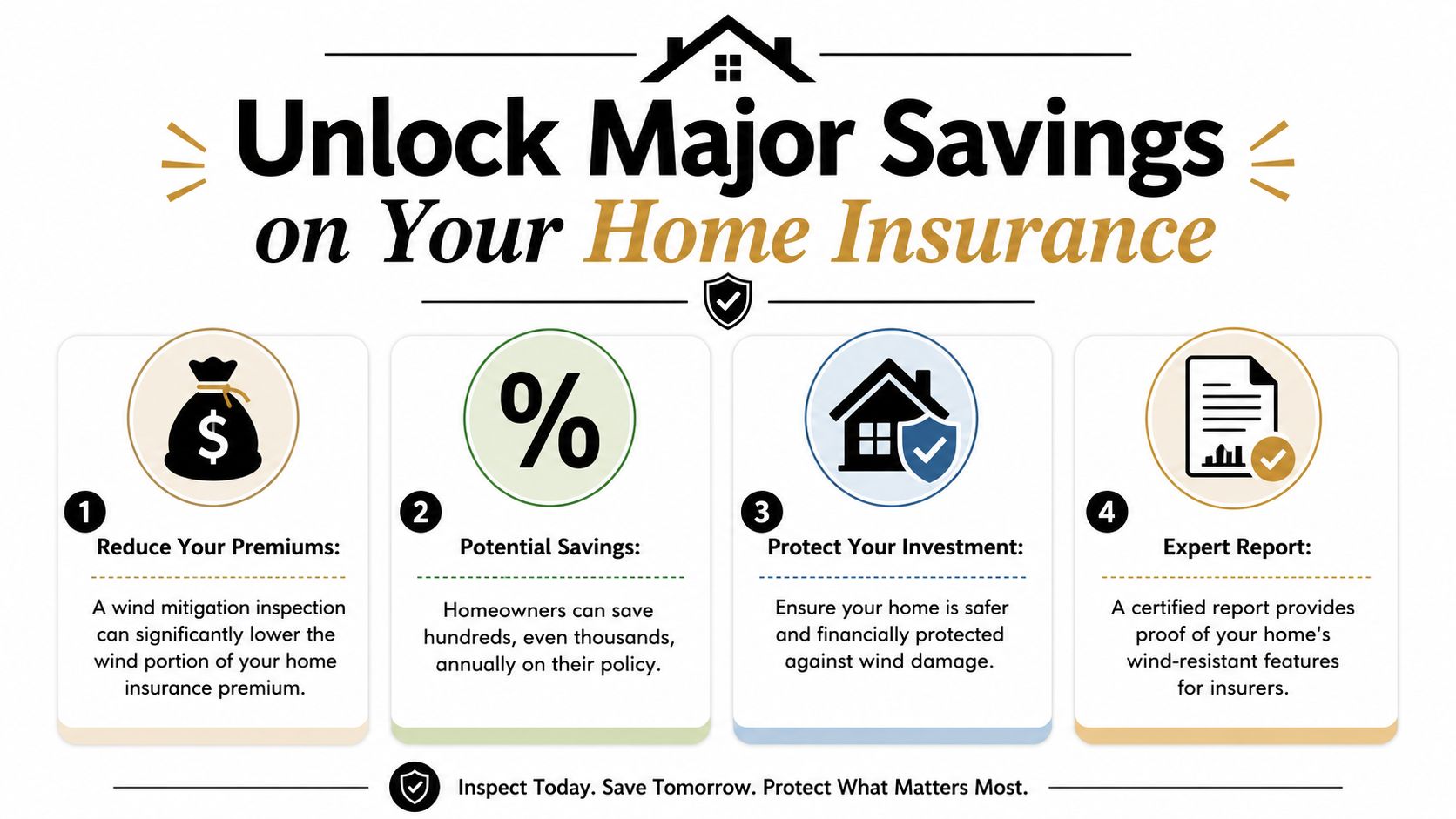

Unlocking Major Savings on Your Home Insurance

In Florida, the wind portion of a homeowner's premium can represent up to 70% of the total premium, and a wind mitigation inspection typically costs $75 to $150 while annual savings can range from $200 to $1,500, often offsetting the inspection cost within the first six months, according to InterNACHI's Florida wind mitigation overview.

That cost-to-savings gap is why this inspection makes so much sense. Few services tied to homeownership have that kind of straightforward payoff. You pay a relatively small amount once, and if the house qualifies, the savings continue year after year while the report remains active.

Where the savings come from

Insurers don't reward a home because it "looks strong." They want documented features tied to wind resistance. When the report shows qualifying items, the carrier can apply credits to the windstorm portion of the policy.

Typical savings drivers include:

- Roof shape: Certain roof geometries handle wind better than others.

- Roof-to-wall connections: Metal connectors hold the roof structure to the walls more effectively than older, weaker attachment methods.

- Opening protection: Impact-resistant or properly rated protective systems reduce the chance of wind entering through broken glass or failed doors.

- Better roof assembly details: The more complete the load path and moisture defense, the more likely the home is to earn meaningful credits.

A carrier can't discount what hasn't been verified. That's the real reason this inspection saves money.

Why this beats guessing

A lot of homeowners assume their insurance company can tell what the house has from the age of the home or from a prior permit record. Sometimes that information helps. It usually isn't enough by itself. The insurer wants the official inspection form completed by a qualified inspector.

Here's the practical trade-off. If the home has good features, the inspection often pays for itself quickly. If the home doesn't have those features, you still learn exactly where the weak spots are before the next storm season. Either way, you get clarity.

| What homeowners often assume | What actually matters |

|---|---|

| "My roof is newer, so I should get every discount." | The insurer needs verified construction details, not just age. |

| "If the windows look strong, that should count." | Opening protection has to be documented correctly. |

| "My agent can figure it out without an inspection." | Credits usually depend on the completed form. |

The other benefit is less obvious, but it matters. Once you know what your house has, you can make smarter upgrade decisions. Instead of spending money blindly, you can target the items that affect wind resistance and insurance pricing.

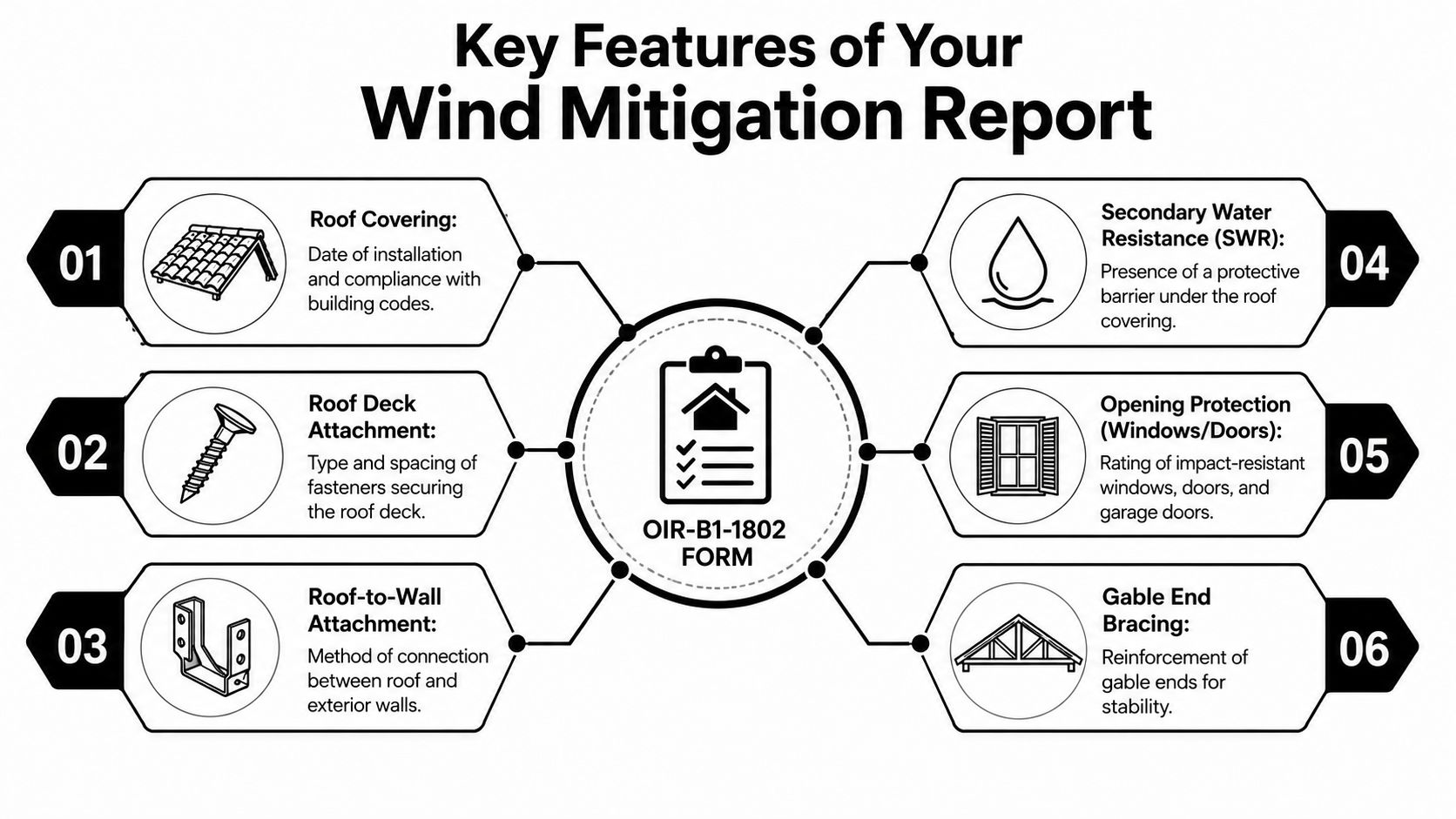

The Key Features of a Wind Mitigation Report

A Florida wind mitigation report centers on six structural attributes recorded on the uniform form: roof covering, roof-deck attachment, roof-wall attachment, roof geometry, opening protection, and the year of construction, as explained in Kin's windstorm mitigation inspection guide. The same source notes that for asphalt shingles to resist winds over 130 mph, the standard calls for specific underlayment and fasteners with minimum 1-inch diameter caps.

What goes on the form

The form isn't guessing. It's a checklist backed by photos, field observations, and visible construction details.

Here's what each category means in plain English:

- Roof covering: This records what roof material is installed and whether it meets the applicable standards tied to the home's age and code path.

- Roof-deck attachment: This is about how the plywood or OSB roof deck is fastened to the framing. Think of it as the grip between the skin of the roof and the bones underneath.

- Roof-wall attachment: These are the connectors that tie the roof framing to the walls. The simplest analogy is a seatbelt for the roof. In strong wind, that connection helps keep lift forces from peeling the roof structure away.

- Roof geometry: Shape matters. Some roof designs shed wind pressure better than others.

- Opening protection: This covers impact-rated windows, doors, garage doors, and other protected openings.

- Year of construction: This helps determine which Florida Building Code version applied when the home was built.

Why roof deck attachment matters so much

From a roofing standpoint, roof-deck attachment is one of the most important sections on the form. Wind doesn't only push sideways. It also creates uplift. That uplift tries to pull the roof assembly apart from the top down.

If the deck fastening is weak, the roof can fail in layers. First the covering takes damage, then the decking starts to let go, then water gets in fast.

The strongest shingles in the world won't save a poorly attached roof deck.

For higher-wind conditions, fastener details matter. The underlayment and cap fastening standards noted above are there for a reason. They help the roof system resist suction forces and keep water out if the outer layer gets compromised.

A homeowner doesn't need to memorize every technical detail. But you should understand the basic principle: the inspection rewards assemblies that stay connected under pressure.

What inspectors usually need to see

An inspector is looking for visible evidence. That can mean attic access, photos of connectors, documentation on impact products, and close review of roof details.

Common photo targets include:

- Metal clips or straps

- Nail patterns at the roof deck

- Window or door labels

- Roof shape from exterior views

- Signs of secondary water protection where visible

This is why a clean report depends on access and documentation. If the feature exists but can't be verified, it may not help you on paper.

Your Step by Step Inspection Guide

A Florida wind mitigation inspection typically takes around one hour, the OIR-B1-1802 form stays valid for exactly five years if there are no material changes to the structure, and new inspections must use the updated 2026 form, according to this Florida wind mitigation inspection explanation.

What happens before the inspector arrives

The prep is simple. The goal is access.

A homeowner should make it easy for the inspector to reach the areas that matter most:

- Attic access: Clear the hatch and the space below it.

- Garage and exterior doors: Make accessible what needs to be opened or viewed.

- Windows and shutters: Have any paperwork available if you kept product labels or permits.

- Roof paperwork: If you have reroof permits or product documents, keep them handy.

You don't need to stage the house like a showing. The inspector isn't grading housekeeping. They need a clear path to key structural areas and enough light to document what they see.

What happens on inspection day

The inspector works through the home methodically. Expect photos, measurements, and a lot of attention to roof-related details. In many homes, the attic tells the most important part of the story.

A normal visit includes review of:

- Roof system details visible from outside and, where accessible, from inside the attic.

- Attachment points like clips, straps, or other roof-to-wall connectors.

- Openings such as windows, entry doors, and garage doors.

- Construction information needed to complete the form accurately.

Bring up any upgrades you've made. A reroof, new impact openings, or added protection can change the outcome if the inspector can verify it.

After the inspection, you receive the completed form and submit it to your insurance agent or carrier. That's the step that turns the inspection into actual savings.

One important detail gets missed all the time. The report may be valid for five years, but if you replace the roof or make other qualifying upgrades before that period ends, it's smart to order a new inspection right away so the updated features can be reflected on the form.

Sample Findings What Inspectors Photograph

The best way to understand a wind mitigation inspection is to think in side-by-side examples. Inspectors aren't taking random photos. They're building a visual record that supports the credits on the form.

A strap beats a toenail connection

One of the clearest examples is roof-to-wall attachment.

If an inspector photographs a proper metal strap or clip that connects the truss or rafter to the wall structure, that usually tells a much stronger story than an older toenail connection. A toenail connection is basically nails driven at an angle to hold framing together. It works, but under wind uplift it doesn't offer the same resistance as dedicated metal hardware.

From a roofer's point of view, this is one of the easiest analogies in the whole inspection. A strap is like buckling the roof down. Toenails are more like hoping friction does enough.

Labels and layers that change the result

Another common photo set involves opening protection. An inspector may photograph labels on impact-resistant windows, doors, skylights, or garage doors. Without a visible label or acceptable documentation, a homeowner can have a strong product installed and still have trouble getting credit for it.

The same thing happens with secondary water resistance. When inspectors can verify that backup barrier under the roof covering, that can make a real difference because it helps limit water intrusion if the outer roofing layer fails.

Florida homeowners average 10% to 45% off their windstorm premium after implementing specific mitigation improvements and submitting a verified report, and the highest-value upgrades include Opening Protection and Secondary Water Resistance, according to Slide Insurance's explanation of wind mitigation inspections.

A few findings inspectors often document:

- Good evidence: Clearly visible hurricane clips, readable impact labels, and visible proof of enhanced roof assembly details.

- Weak evidence: Painted-over connectors, missing labels, blocked attic access, or improvements the owner remembers but can't document.

- Upgrade opportunities: Better opening protection and added moisture defense under the roof covering often give homeowners the most practical path to better credits.

If you improve the house after the inspection, update the report. Old photos won't capture new value.

That's one of the most common missed opportunities. Homeowners spend money on a better roof or better openings, then keep using an older report that doesn't reflect the upgrade.

Schedule Your Inspection with Paletz Today

When it's time to get the form done correctly, licensing matters as much as roofing knowledge. Florida requires qualified inspectors to hold specific credentials, such as certain contractor licenses, professional engineering licenses, or certified building code inspector status, and they must also pass a state-required training program to legally complete the OIR-B1-1802 form, as outlined in the Florida wind mitigation booklet.

Why licensing matters

This isn't a form you want filled out casually. Small mistakes can cost you credits. Missed photo documentation can cost you credits. An inspector who doesn't understand roofing assemblies can overlook details that matter.

Paletz Roofing and Inspections serves South Florida with deep field experience in reroofing, repairs, and inspections, which matters because wind mitigation isn't just paperwork. It's applied building knowledge. Their background across Broward, Miami-Dade, and Palm Beach counties gives homeowners a practical advantage when the home has older roof systems, mixed upgrades, or details that need careful documentation.

You can see the company branding and service presence through the Paletz Roofing and Inspections logo asset, but the bigger point is credibility in the field. A qualified inspector needs to know what to look for, how to photograph it, and how to document it so the carrier can use it.

{kind=link}

Local experience counts

South Florida homes aren't all built the same. Some have older framing details. Some were reroofed under different code eras. Some have impact windows on part of the home but not all of it. That mix is where experience shows.

If you're ready to get clear documentation and find out whether your house qualifies for credits, Paletz Roofing and Inspections is a practical place to start. They know the local housing stock, the inspection process, and the standards that matter to insurers.

Frequently Asked Questions About Wind Mitigation

Can a wind mitigation inspection raise my premium

No. A wind mitigation inspection is designed to find and document features that can save money. It cannot raise premiums or disqualify a home from coverage, which is exactly why many inspectors describe it as a premium saver. The confusion usually comes from the 4-point inspection, which is a different inspection entirely, as explained in this video breakdown of wind mitigation versus 4-point inspection outcomes.

Here's the clean distinction:

- Wind mitigation inspection: Focuses on wind-resistant features and discounts.

- 4-point inspection: Reviews major systems like roof, electrical, plumbing, and HVAC from an underwriting perspective.

- Big difference: A 4-point inspection can lead to repair demands or pricing changes because the insurer is evaluating risk acceptance, not just credits.

That difference matters for new buyers. People hear "inspection" and assume both reports do the same job. They don't.

Wind mitigation asks, "What protective features does this house have?" A 4-point asks, "Are the major systems acceptable to insure?"

How long is the report valid

A wind mitigation report stays valid for five years if there are no material changes to the structure. But don't let that five-year window fool you into waiting after an upgrade.

If you install a new roof, replace windows, or add other qualifying mitigation improvements, order a new inspection so the report reflects the better features. An old report can leave savings on the table because the carrier only sees what the current form documents.

Do I need to be home

Usually, yes. The inspector often needs access to the attic and other parts of the property. The visit itself is typically short and doesn't usually disrupt the home. Another practical point is that utilities don't need to be on for this inspection, which makes it easier to schedule around move-ins or vacant properties, according to Noble Public Adjusting Group's overview of Florida wind mitigation inspections.

What should I ask before any inspection

Good questions save time. Ask what access is needed, whether attic entry is required, what documents might help, and how the final report will be delivered. If you're buying a home and want a useful checklist for the broader inspection conversation, this roundup of Saleswise home inspection advice is a solid place to start.

For wind mitigation specifically, the best homeowner mindset is simple. Give the inspector access, provide any upgrade paperwork you have, and make sure the final report goes to your agent or insurer promptly.

If you want clear answers, proper documentation, and local roofing experience behind the inspection, contact Paletz Roofing and Inspections to schedule your wind mitigation inspection and see what savings your home may qualify for.