Filing a roof damage insurance claim in Palm Beach FL isn't just another home repair task. It's a high-stakes process shaped by our intense local weather and some of the strictest insurance laws in the country. This isn't just about paperwork; it's about protecting your biggest investment after a storm has done its worst.

The Unique Challenges of Palm Beach Roof Claims

Navigating a roof damage claim in Palm Beach County feels different because, frankly, it is. We're not just talking about a few shingles blown off on a windy day. We live in a region that's constantly in the crosshairs of hurricanes, tropical storms, and brutal thunderstorms that can drop hail the size of golf balls.

That constant threat creates an entirely different environment for both homeowners and insurance companies.

The moment you spot water stains spreading across your ceiling or see daylight peeking through your attic, the pressure is on. It's an overwhelming feeling. Your home feels exposed, and the path to getting it fixed seems incredibly complicated. This is exactly why understanding the local landscape is your best first defense.

Weather and Local Insurance Realities

Insurers down here in South Florida are on constant high alert. They process a staggering volume of claims and have created specific protocols just for storm-prone areas like ours. The main culprits for roof damage here aren't typical wear and tear—they're major weather events.

- Hurricanes: A hurricane triggers a special "hurricane deductible." This is a big deal. It's not a flat amount but a percentage of your home's total insured value, which can easily mean thousands of dollars out-of-pocket before your policy kicks in.

- Tropical Storms: Even the storms that don't earn a hurricane name can pack a punch. They bring torrential rain and sustained winds strong enough to peel back shingles and compromise your roof's entire structure.

- Hail Storms: We get sudden, violent hailstorms that can create hundreds of small fractures and dents across your roof. The real danger here is that they lead to slow leaks you might not even discover for months. You can see examples of this type of damage in our photo gallery of past projects. https://paletzroofing.com/wp-content/uploads/2025/09/thumbnail-17-768×432.jpg

{kind=link}

The sheer volume of claims is mind-boggling. After major storms like Hurricane Michael, Florida insurers reported paid losses topping $8.5 billion. You’re not just filing a claim; you’re entering a system dealing with billions in damages.

Here's the key takeaway: Your policy is more than a simple contract. It's a complex legal document with very specific definitions for "hurricane windstorm," which can even include tornadoes miles away from the eye. This directly impacts which deductible applies to your claim.

Navigating the Post-Storm Process

What you do in the immediate aftermath of a storm is critical. It sets the stage for your entire claim.

It’s about more than just calling your insurance agent. For instance, significant roof repairs almost always require navigating local building permit requirements, which can be particularly strict in hurricane zones like Palm Beach County.

Your immediate focus should be twofold: stop any further damage from happening, and start building a rock-solid case for your claim. The good news is, you don't have to figure it out alone. This guide is your roadmap, designed to walk you through every step—from that first shocking moment of discovery to cashing the final settlement check.

Documenting Your Damage to Build an Airtight Claim

When you're filing a roof damage insurance claim, your photos and records are your most powerful currency. They aren't just pictures; they are undeniable proof that turns a simple request into a compelling case for full compensation. Building an airtight claim starts the moment you suspect damage, and it takes a bit more strategy than just snapping a few quick shots on your phone.

Your goal is to build an evidence file that leaves no room for doubt or dispute. You're telling a story with visuals and documents—the story of your roof before the storm, the immediate aftermath, and the hidden consequences that can pop up later. This isn't just for you; it's the primary evidence an adjuster will use to figure out what your claim is worth.

Creating a Visual Timeline of the Damage

Get your camera out immediately, even before you've called your insurer. The key is to capture everything from multiple perspectives, starting wide and then zooming in on the details.

Think like a detective piecing together a crime scene. Your first photos should be wide-angle shots of your entire property. Get all sides of your house to show how the roof fits with the rest of the structure and the yard around it. These images set the scene and can help prove the damage was widespread and consistent with a major weather event.

Now, it's time to get closer. Go over each section of the roof methodically, looking for the specific kinds of damage that adjusters are trained to spot.

- Lifted or Missing Shingles: Get clear photos of any shingles that are curled, creased, lifted, or completely gone. If you can do it safely, put a ruler or a coin next to the damage to give it a sense of scale.

- Hail Impact Marks: For hail damage, look for dents or pockmarks on shingles, vents, and gutters. These can be tough to see, so try taking photos at different times of day when the light creates shadows that make the impressions pop.

- Granule Loss: After a storm, you might see a bunch of tiny asphalt granules from your shingles piled up in your gutters or on the ground. Snap a picture of this—it’s a dead giveaway of premature aging and wear caused by the storm.

- Flashing and Seals: Pay close attention to the metal flashing around chimneys, vents, and skylights. Damage here is one of the most common ways water finds its way in.

After you've covered the exterior, head inside. Water damage doesn't always show up right away. Check your attic for damp insulation, dark spots on the wood rafters, or any other signs of moisture. In the main house, photograph any water stains on ceilings or walls, no matter how small they seem. These interior shots are what directly link the roof damage outside to the financial loss inside your home.

The Power of Pre-Storm Evidence

One of the most effective things you can do is create a clear "before-and-after" story. Insurers love to argue that damage was already there or was just normal wear and tear. It’s your job to prove them wrong.

Pull together any records you have on your roof's history. This could be the original installation receipt, invoices for repairs, or records from recent maintenance inspections. These documents establish your roof's age and condition before the storm hit, making it much harder for an insurer to claim the damage was your fault. Think of it as establishing a baseline of good condition. This kind of detailed evidence, like inspection records, can make a huge difference. https://paletzroofing.com/wp-content/uploads/2025/09/thumbnail-18-768×432.jpg

{kind=link}

Pro Tip: Timestamp everything. Most smartphones automatically embed the date and time into photos, but double-check that this feature is turned on. For any paper documents, get in the habit of writing the date you collected them. This creates an organized, chronological file that’s easy for both you and the adjuster to follow.

Why This Level of Detail Is Non-Negotiable in Palm Beach

Let's be honest: the insurance game in Florida has gotten tougher for homeowners. The number of roof damage insurance claims in Palm Beach has skyrocketed, thanks to a combination of severe weather, inflation, and fraud. Industry experts will tell you this has put immense pressure on insurance carriers, forcing them to get much stricter with their rules.

For example, some insurers now require claims to be filed within 365 days and have set minimum hail size thresholds just to qualify. This makes your meticulous documentation more critical than ever. You can dig into more insights on this claims crisis over at nicb.org.

Your detailed evidence file is your first line of defense against a claim denial or a lowball offer. When an adjuster sees a well-organized, thoroughly documented claim, it sends a clear signal that you're a serious and prepared policyholder. It takes away their wiggle room to question the cause or extent of the damage, paving the way for a much smoother and fairer settlement process.

Filing Your Claim and Communicating with Your Insurer

Once you have all your documentation squared away, it’s time to officially start your roof damage insurance claim in Palm Beach, FL. That first phone call is more important than most people think; it really sets the tone for everything that follows. If you approach it with confidence and all your facts in order, you'll find the whole process goes a lot smoother.

Think of this initial contact less like just reporting damage and more like opening a negotiation where you're the one holding all the cards.

Making the First Contact

Before you even think about dialing your insurance company, get your key information laid out right in front of you. Fumbling around for your policy number or the date of the storm doesn't make a great first impression and can even lead to mistakes.

Your Pre-Call Checklist:

- Policy Number: This is the very first thing they’ll ask for. Have it ready.

- Date and Time of Loss: Be as specific as you can. Note the exact date the storm hit or when you first noticed the damage.

- A Brief Description of Damage: Stick to the facts you’ve documented. Something simple like, "My roof was damaged by high winds during the storm on October 15th. I have missing shingles and an active leak in my attic."

- Your Contact Information: Double-check that they have the best phone number and email to reach you.

When you get a representative on the line, stay calm and professional. Just state the facts clearly. Avoid getting emotional or guessing what the repairs might cost—that comes later. Your only job right now is to report the loss accurately. Before you hang up, they will give you a claim number. This is your magic number. Write it down and keep it somewhere safe, as you’ll need it for every single conversation from here on out.

The Role of Your Assigned Adjuster

Shortly after you file, you’ll be assigned a claims adjuster. This person is the key player from the insurance company's side. It's their job to investigate your claim, figure out how bad the damage is, and decide how much the insurance company should pay based on your policy.

It's crucial to remember that while most adjusters are professional, their loyalty is to their employer—the insurance company. They work within the insurer's financial interests and guidelines, which is precisely why your detailed documentation and clear communication are so important.

A huge win for Florida homeowners came with Senate Bill 2-D. This law put stricter deadlines on insurers. They now have 14 days to acknowledge your claim and 90 days to make a decision (pay or deny), unless there are circumstances beyond their control. This is a game-changer that helps prevent claims from dragging on forever.

Maintaining a Meticulous Communication Log

Starting with that very first phone call, you need to document everything. This isn't just a suggestion; it’s one of the most powerful things you can do to protect yourself. Grab a notebook or start a new document on your computer and create a log for every single interaction.

What to Record for Every Communication:

- Date and Time: Log every call, email, and letter.

- Person's Name and Title: Always ask for the full name and job title of whoever you're talking to (e.g., "Jane Doe, Senior Claims Adjuster").

- Summary of Discussion: Jot down the key points. What did you talk about? What did they promise to do? Did they give you any deadlines?

- Reference Numbers: Always include your claim number on any emails or letters you send.

This log becomes your proof. If a dispute comes up later about what was said or promised, you won’t be relying on memory. You’ll have a detailed, factual record of every conversation.

Your Presence During the Adjuster's Inspection

The adjuster will need to schedule a time to come out and inspect your roof. Your presence during this inspection is absolutely non-negotiable. Don’t let them walk your property alone. This is your chance to be an active part of the process.

Walk the property with the adjuster, using your own photos and notes as a guide. You can politely point out every bit of damage you found, from the hail dents on the flashing to that new water stain on the ceiling inside. This makes it impossible for things to be "overlooked." By being there, you shift from being a passive victim to an informed homeowner who is managing their own claim. It makes it much harder for legitimate damage to be downplayed or dismissed.

Navigating the Adjuster Inspection and Repair Estimates

The insurance adjuster's visit is the make-or-break moment for your roof damage claim here in Palm Beach. Seriously, this one meeting can swing your settlement by thousands of dollars. This isn't a time to sit back and watch; you need to be an active, prepared participant.

Your insurance company will send out an adjuster to assess the damage. They'll either be a staff adjuster (who works directly for the insurer) or an independent adjuster (a contractor they hire, especially after a big storm). It doesn't really matter which one shows up—their job is to evaluate the damage from the insurance company's perspective.

Getting Ready for the Adjuster's Visit

Here’s the single most important thing you can do before that adjuster even schedules their visit: get your own repair estimates. Call at least two, preferably three, reputable and licensed Palm Beach roofing contractors. Ask them for detailed, line-item quotes for a complete roof repair or replacement. This isn't just a good idea; it's the foundation of a strong claim.

Walking into that meeting with professional estimates completely changes the dynamic. You're no longer just accepting what the adjuster says as fact. Instead, you're comparing their professional opinion against real-world quotes from local experts who work on roofs like yours every day. This gives you immediate, powerful leverage to challenge any lowball numbers.

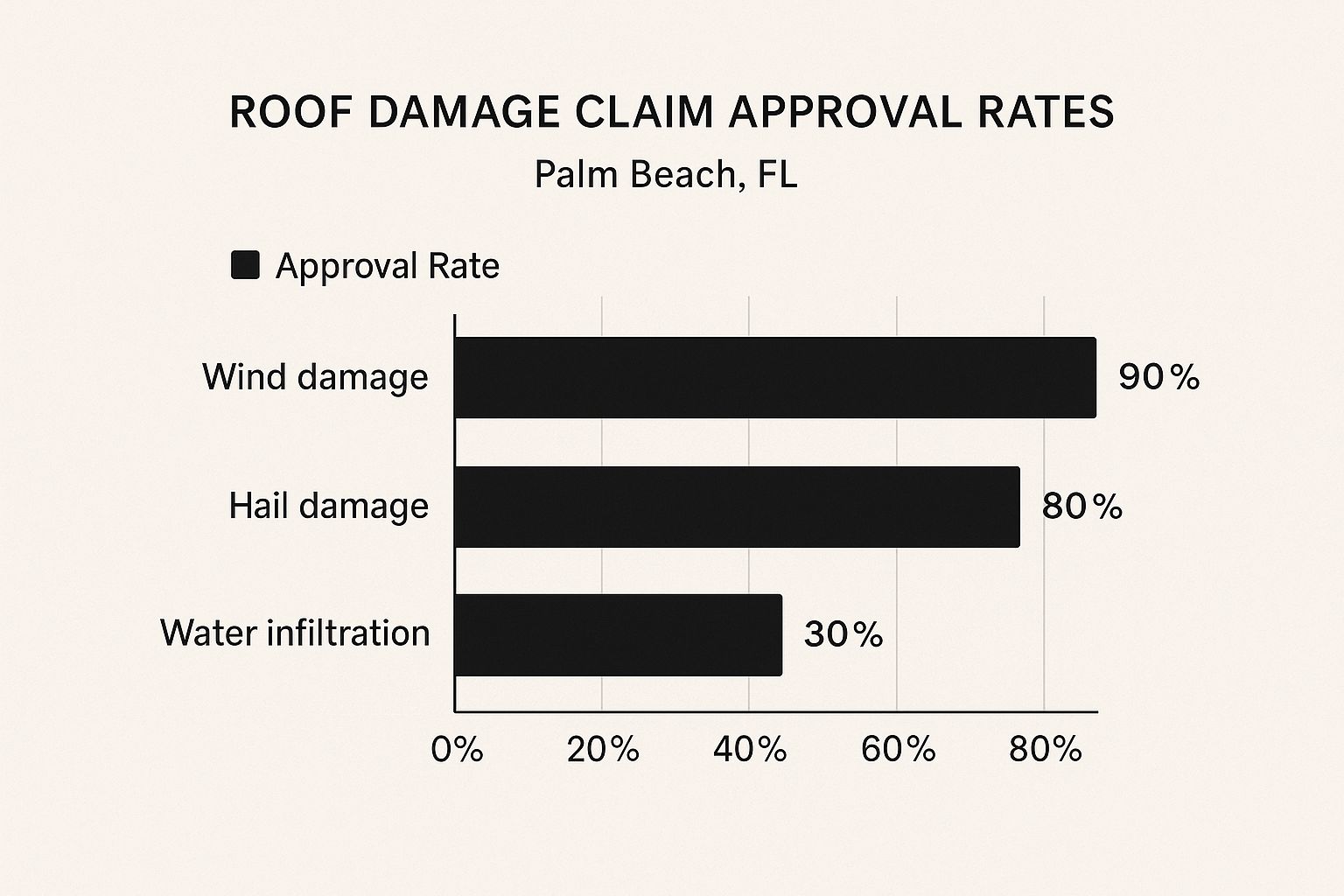

The infographic below shows just how much the type of damage can affect the outcome of a claim in our area, which is why having your ducks in a row is so crucial.

As you can see, claims for obvious wind damage tend to get approved more easily. But when you're dealing with issues like slow leaks or water infiltration, insurers put things under a much bigger microscope, making your detailed documentation absolutely vital.

Comparing Estimates: Adjuster vs. Contractor

After the inspection, the adjuster will give you their report, sometimes called a "scope of loss." Now it's time to sit down and compare it, line by line, with the quotes from your local roofers. Don't just glance at the final dollar amount. The details are where insurers often cut corners.

When you're comparing these documents, you need to play detective. It’s common to see major differences between what an adjuster offers and what a local contractor knows it will actually cost to do the job right.

Comparing an Adjuster's Estimate vs a Contractor's Bid

| Line Item | What to Look For in the Adjuster's Estimate | What a Contractor's Bid Should Include |

|---|---|---|

| Scope of Work | Does it cover a full replacement or just a "patch job"? Adjusters may only account for the obviously damaged sections. | A comprehensive plan for a full replacement if necessary, including tear-off, underlayment, flashing, and ventilation. |

| Material Costs | Are they using generic, low-cost materials (e.g., standard 3-tab shingles) or pricing for the actual materials on your roof? | Specific, brand-name materials that match the quality and style of your existing roof (e.g., architectural shingles). |

| Labor Rates | Are the rates based on a national average, or do they reflect the real cost of skilled labor here in Palm Beach County? | Localized labor rates that account for our area's cost of living and the demand for qualified roofers. |

| Code Upgrades | Is there an allowance for bringing the roof up to current Florida Building Code standards? This is often missed. | Any necessary code-required upgrades, such as new decking, hurricane straps, or improved underlayment. |

| Overhead & Profit | Does the estimate include Overhead and Profit (O&P)? This is a standard, legitimate cost (10% and 10%) that insurers sometimes "forget." | A clear line item for O&P, which covers the contractor's operational costs and is a standard part of any construction bid. |

Looking at this breakdown, you can see how an initial offer might fall short. A contractor's bid is based on the reality of completing the work in your specific location, while an adjuster's estimate is often built using generalized software that may not capture the full picture.

This is exactly why you want a contractor who knows the insurance game. They speak the same language as adjusters and can spot missing or underfunded items in a scope of loss in minutes. To get a sense of what a truly thorough inspection looks like, check out this detailed roof inspection process from our team at Paletz Roofing.

{kind=link}

The "Matching" Issue in Florida Law

One of the biggest arguments you might face is over "matching." Let's say a storm damages half of your roof, but the shingles on it were discontinued five years ago. You can't just slap on a new, mismatched section—it would look terrible and tank your home's value.

Thankfully, Florida law is on your side. State regulations often require an insurer to pay for the replacement of undamaged sections to ensure a reasonably uniform appearance. If a matching shingle is truly unavailable, this can mean they are responsible for a full roof replacement, not just the part that was hit.

Be ready for a fight on this one. The adjuster’s first move will likely be to offer to pay for only the damaged slope. This is where your contractor's bid, which should clearly state the need for a full replacement due to matching issues, becomes your most powerful piece of evidence.

If you find big gaps between the adjuster's offer and your contractor's bids, don't worry. This is a normal part of the process. The first offer is simply a starting point for negotiation. Your next step is to professionally present your evidence—the photos, the documentation, and the contractor quotes—and start a conversation about why their numbers don't reflect the real-world cost of making you whole. A calm, well-documented argument backed by local experts is your best strategy for getting a fair settlement.

What To Do When Your Claim Is Denied Or Underpaid

Getting a denial letter—or a lowball offer that barely covers materials—can feel like a gut punch after you’ve weathered a storm. As any Palm Beach homeowner knows, it’s the last thing you need when you’re already dealing with damage and stress.

Florida homeowners face this all too often. In 2022, our state recorded the lowest claim payment rate in the country, with over a third of all claims closed without a single dollar paid. Major carriers such as State Farm Florida and Allstate subsidiaries denied nearly 50% of their roof‐damage claims. Even local audits in Palm Beach Gardens flagged insurers rejecting more than 46% of homeowner claims.

Don’t let that initial “no” be the end of your story. Insurers’ first decision often leans in their favor—based on a single adjuster’s snapshot. Your job now is to dig in, clarify the reasons, and respond with precision.

Decoding The Denial And Demanding Answers

Begin by formally requesting the insurer’s written explanation for the denial or low settlement. A vague phone summary won’t cut it—you need that letter in hand.

That letter will reference specific policy language or exclusions. Typical justifications for denied roof claims in Palm Beach include:

- Pre-Existing Damage: The insurer maintains the damage predates the storm.

- Improper Maintenance: They argue you failed to keep up with routine repairs.

- Hurricane Deductible Issues: Repair costs fall below your high deductible.

- Policy Exclusions: Certain water infiltration or structural issues aren’t covered.

With the denial letter as your roadmap, pull together your own evidence—storm photos, contractor estimates, maintenance logs—and craft a point-by-point rebuttal. If negotiations stall, learning how to appeal an insurance denial can open a strategic path forward.

Bringing In Professional Reinforcements

Facing a multi-billion-dollar insurer alone is overwhelming—they’ve got adjusters, attorneys, and deep pockets on standby. That’s why many homeowners call in outside help to even the odds.

-

Public Adjusters

These state-licensed professionals work solely for you, the policyholder. They handle every aspect of your claim—documentation, negotiations, calls—and take a contingency fee based on the settlement they secure. -

Insurance Claim Attorneys

When an insurer crosses into bad faith—unreasonable delays, misrepresenting your coverage, or outright refusing a valid claim—an attorney has the legal muscle to sue for your full damages and additional penalties.

Making The Right Choice:

For a straightforward dispute over valuation, a public adjuster is often the ideal first step. If your insurer digs in or violates Florida law, an attorney can escalate the fight and compel compliance.

A denial isn’t a dead end—it’s an invitation to escalate. By pinpointing the insurer’s reasoning and, if needed, enlisting experts, you stand a strong chance of turning that initial “no” into a full, fair settlement.

Common Questions About Palm Beach Roof Claims

When your Palm Beach roof is damaged, the questions can start piling up faster than the storm clouds. The whole world of insurance claims feels like it has its own language, full of confusing jargon and complicated rules. We're here to cut through the noise with clear, straightforward answers to the questions we hear from homeowners every day.

How Long Do I Have to File a Roof Claim in Florida?

This is probably one of the most critical questions, and the clock is always ticking. Florida law is very specific about the deadlines for filing property damage claims after a storm. For damage from a hurricane or major windstorm, you have a limited window from the day the damage happened to get your claim officially reported to the insurance company.

These timelines can shift with new laws, which is why the most important thing you can do is act fast. As soon as it's safe, get the damage on record with your insurer. You don't want to risk missing that deadline.

Will Filing a Claim Make My Insurance Rates Go Up?

It's a completely fair question and a major worry for most homeowners. The good news is that Florida law offers a pretty significant protection here. An insurance company is legally barred from jacking up your individual premium or dropping you just for filing a single claim caused by an "Act of God," which absolutely includes hurricanes and other big storms.

Now, if a monster hurricane tears through Palm Beach County causing widespread, massive losses, insurers might ask for a general rate increase for everyone in the area. But that would happen whether you filed a personal claim or not.

The key takeaway is this: A potential rate hike would be regional, not a personal penalty for using the policy you've been paying for. Your individual claim for storm damage is protected.

What Exactly Is a Hurricane Deductible?

Your hurricane deductible is a different animal altogether from your regular, everyday deductible. It only kicks in for damage caused by a storm that the National Hurricane Center has officially named a hurricane.

Instead of a simple flat dollar amount, it's almost always a percentage of your home's total insured value—often 2%, 5%, or even 10%.

Let's put that into real numbers:

- On a home insured for $500,000, a 2% hurricane deductible means you're on the hook for the first $10,000 of repairs.

- With a 5% deductible on that same home, your out-of-pocket cost skyrockets to $25,000.

This can be a massive financial shock if you aren't prepared for that kind of upfront expense before your insurance coverage even starts paying.

Should I Hire a Public Adjuster for My Roof Claim?

A good public adjuster can be an absolute game-changer, especially if you're dealing with a large, complicated, or disputed claim. These are professionals licensed by the state who work for one person and one person only: you, the policyholder. They don't work for the insurance company.

Their entire job is to take over the claim for you. They document the damage, handle all the back-and-forth with the insurer, and negotiate the best possible settlement. They get paid a percentage of the final claim amount they win for you. For a small, straightforward claim where the insurance company's first offer seems fair, you might not need one. But if you’re staring down a denial, a lowball offer, or you just feel completely in over your head, they can be a powerful advocate to have in your corner.

Trying to navigate a roof damage insurance claim in Palm Beach FL is a tough road, but you shouldn't have to walk it alone. The team at Paletz Roofing and Inspections has more than 30 years of experience helping homeowners get their lives back to normal. For a free, no-obligation inspection and some honest advice on what to do next, visit us at https://paletzroofing.com.