The surprising part about commercial roof maintenance isn't the work. It's the math. A structured plan on a typical 20,000-square-foot building often runs only $1,200 to $1,600 per year when it includes two thorough inspections, based on the common $0.03 to $0.04 per square foot per visit pricing band cited in commercial roof maintenance pricing guidance. In South Florida, where wind, heat, rain, and insurance scrutiny all hit harder, that's not a line item to avoid. It's one of the cheaper ways to protect a building.

New property managers often inherit roofs the same way they inherit parking lots, chillers, and tenant complaints. Without fanfare. Then the first hard rain exposes every deferred decision. The roof that looked fine from the ground starts leaking around a curb, water reaches insulation, a tenant calls, an insurer asks for records, and suddenly the “savings” from skipping maintenance disappear.

That's why commercial roof maintenance plans matter here more than in easier climates. In South Florida, they aren't a nice operational habit. They're part asset protection, part storm-readiness discipline, and part documentation system for warranties, claims, and future budgeting.

Table of Contents

- Your Commercial Roof Is an Asset Not an Expense

- Defining Proactive Roof Asset Management

- Key Components of a Comprehensive Maintenance Plan

- Calculating the ROI of Your Maintenance Plan

- Understanding the Costs of a Commercial Roof Plan

- Selecting a Roofing Partner for South Florida Properties

Your Commercial Roof Is an Asset Not an Expense

A commercial roof usually gets treated like a problem only after it leaks. That's backwards.

The roof is a capital asset sitting over inventory, tenants, equipment, wiring, finished interiors, and day-to-day operations. When it fails during a storm cycle or a busy tenant period, the cost doesn't stay on the roof. It spreads into overtime labor, interior cleanup, service interruptions, unhappy occupants, and rushed decision-making.

A better way to look at it is this. Reactive roof spending is chaotic spending. Planned roof spending is controlled spending.

One scenario plays out all the time. A manager delays inspections because the roof “isn't leaking.” Months later, water shows up inside near an HVAC curb or parapet edge after heavy rain. The contractor who gets called first isn't evaluating long-term roof performance. They're stopping active water intrusion as fast as possible. That's necessary work, but it's also the most expensive mindset to build a program around.

By contrast, a formal maintenance plan creates predictability. Someone checks drains, sealants, penetrations, edge details, field membrane condition, and visible wear before those details turn into interior damage. The roof stays on a schedule instead of becoming a surprise.

Practical rule: If your first call happens after water reaches the inside of the building, you're already paying the premium version of roof management.

South Florida raises the stakes. Heat ages materials. Wind tests attachments and edges. Heavy rain exposes drainage problems fast. A roof can look acceptable from the parking lot and still have vulnerable flashings, clogged drains, or early membrane separation that only shows up under professional inspection.

For many owners, the shift happens when they stop asking, “How much does roof maintenance cost?” and start asking, “What does a roof failure interrupt?” That's the core budget question.

If you need a visual reminder of what's at risk, even a simple commercial roof overview image gets the point across. The roof isn't just a surface. It's the first protective layer over everything the building earns from.

{kind=link}

Defining Proactive Roof Asset Management

A real maintenance plan isn't a guy with a ladder showing up when there's a stain on a ceiling tile. It's a scheduled operating practice.

Think about fleet maintenance. You don't run delivery trucks until one dies on the road and then call that a strategy. You inspect fluids, brakes, tires, and wear items on a schedule because downtime costs more than planned service. Commercial roof maintenance plans work the same way.

A maintenance plan is a program, not a checklist

At minimum, a proactive plan organizes three things:

- Scheduled observation so someone qualified is looking for changes before they become failures.

- Routine housekeeping such as cleaning drains, removing debris, and keeping water pathways open.

- Planned corrective work on small defects like failing sealant, loose flashing, membrane punctures, and edge vulnerabilities.

That structure matters because roofs usually don't fail all at once. They fail at details. Water enters around penetrations, flashings, seams, and drainage points. The visible leak inside may be the last symptom, not the first.

What reactive management gets wrong

Reactive management sounds cheaper because it delays invoices. In practice, it creates three problems.

- Budget instability: Costs show up unpredictably and often at the worst time.

- Operational disruption: Tenants, staff, or customers feel the impact while the repair is happening.

- Incomplete information: Without records, managers can't easily show roof history to insurers, ownership groups, or warranty providers.

That's especially risky on low-slope systems common in South Florida, where standing water, UV exposure, rooftop traffic, and storm events can accelerate failure at the smallest weak points.

Good roof management is boring on purpose. It replaces emergency decisions with scheduled decisions.

Drainage is one of the first tests of whether a plan is serious

A plan that ignores drainage isn't a plan. It's a partial service. Water has to leave the roof quickly, especially in a region where downpours can expose every blocked drain, scupper, and gutter path in one afternoon.

Managers who want to understand the broader discipline behind proactive drain maintenance should pay attention to one principle that carries over directly to roofs: flow problems are cheaper to prevent than to diagnose after backup or overflow.

What proactive roof asset management looks like in practice

A strong plan should feel routine, documented, and specific. You should know:

- When inspections happen

- What areas get checked

- Which minor repairs are included or recommended

- How findings are documented

- Who owns follow-up decisions internally

That's the difference between maintenance theater and actual asset management. One gives you a service visit. The other gives you control.

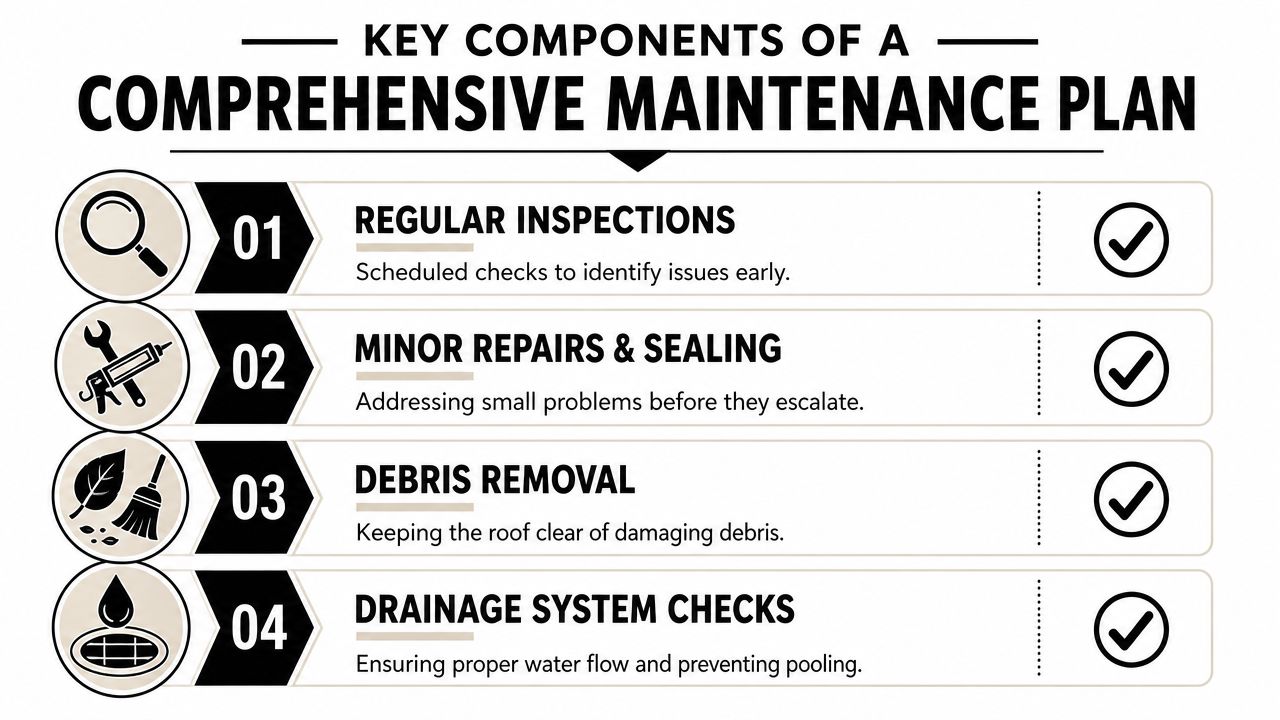

Key Components of a Comprehensive Maintenance Plan

A maintenance proposal should read like a scope of work, not a vague promise. If it only says “inspection and cleaning,” a property manager has no clear service standard, no accountability, and very little protection when the next storm pushes water into the building.

Major industry guidance, including from the National Roofing Contractors Association, recommends that commercial flat and low-slope roofs be inspected at least twice per year, typically in spring and fall, and that cadence can extend useful roof life by up to about 50%, according to commercial roof maintenance guidance. In South Florida, that baseline usually is not enough by itself. Hurricane season, wind-driven rain, insurance scrutiny, and stricter documentation expectations mean post-storm inspections matter too, especially if you may need to support a claim or show that the roof was maintained under warranty requirements.

Here's what a detailed plan should include.

What scheduled inspections actually cover

A proper inspection is systematic. It is not a quick lap around the roof with a phone camera.

The crew should check the field membrane, seams, flashings, penetrations, edge metal, drains, gutters, scuppers, expansion joints, and visible signs of ponding or structural movement. On occupied buildings, the inspection should also note interior staining, damp ceiling tiles, or recurring leak locations, because the water entry point and the visible interior symptom are often several feet apart.

A useful inspection report answers practical questions a manager can act on:

| Area | What the inspection should identify |

|---|---|

| Membrane field | Wear, punctures, open seams, surface deterioration |

| Penetrations | Failing sealant, loose boots, curb vulnerabilities |

| Perimeter and edges | Attachment concerns, metal condition, separation points |

| Drainage components | Obstructions, slow flow, standing water indicators |

| Interior clues | Staining, moisture patterns, recurring leak zones |

That level of reporting helps ownership decide what needs immediate repair, what can be monitored, and what belongs in the next capital planning discussion. It also creates a paper trail that matters in South Florida, where carriers and consultants may ask for dated photos and service records after a storm event.

Why drainage and debris control matter

Water has to leave the roof fast. In South Florida, one blocked drain can turn an ordinary afternoon storm into interior damage, tenant complaints, and a service call that costs far more than routine maintenance.

Debris buildup usually starts small. Leaves, gravel, packaging scraps, screws left by other trades, and HVAC service debris collect around drains and corners. Then flow slows down. Water ponds longer, dirt holds moisture at the laps and flashing lines, and overflow starts pushing toward edges, penetrations, and door thresholds.

A plan should spell out the drainage work, not assume it:

- Drain clearing: Main drains, strainers, and surrounding collection areas

- Scupper review: Openings must stay unobstructed and physically intact

- Gutter cleaning: Built-up material at roof edge lines creates backup fast

- Debris removal: Especially around HVAC units, corners, parapets, and access paths

That work protects more than the roof membrane. It reduces slip hazards, lowers the chance of fascia and wall staining, and helps a manager show that water management was being handled before a claim, inspection, or code-related repair discussion.

The value of small repairs done early

Small repairs are where maintenance plans pay for themselves. A split in sealant, a loose counterflashing, a lifted edge detail, or a puncture from rooftop traffic may look minor today. After one summer storm cycle, that same issue can become wet insulation, deck corrosion, or an active leak above occupied space.

The better plans include a clear process for handling these items while the scope is still small. That means documenting the condition, assigning priority, pricing the repair, and getting approval before the problem spreads.

On South Florida properties, edge details and penetrations deserve close attention because they take the brunt of wind pressure and wind-driven rain. For a visual example of the areas that need that kind of review, this commercial low-slope roof image shows the kind of surface where drainage paths, flashing details, and rooftop traffic points deserve regular attention.

{kind=link}

Documentation is part of the service

Every visit should leave a usable record. A vague email saying the roof was “checked” does not help with budgeting, warranty support, ownership reporting, or an insurance file.

The record should include dated photos, condition notes, repair recommendations, completed work, and any changes made by other trades. If a contractor added equipment, cut a new penetration, or disturbed flashing at a curb, that should be in the file. South Florida owners deal with enough pressure from storms, insurers, and code-driven repair questions already. Missing records only make those conversations harder and more expensive.

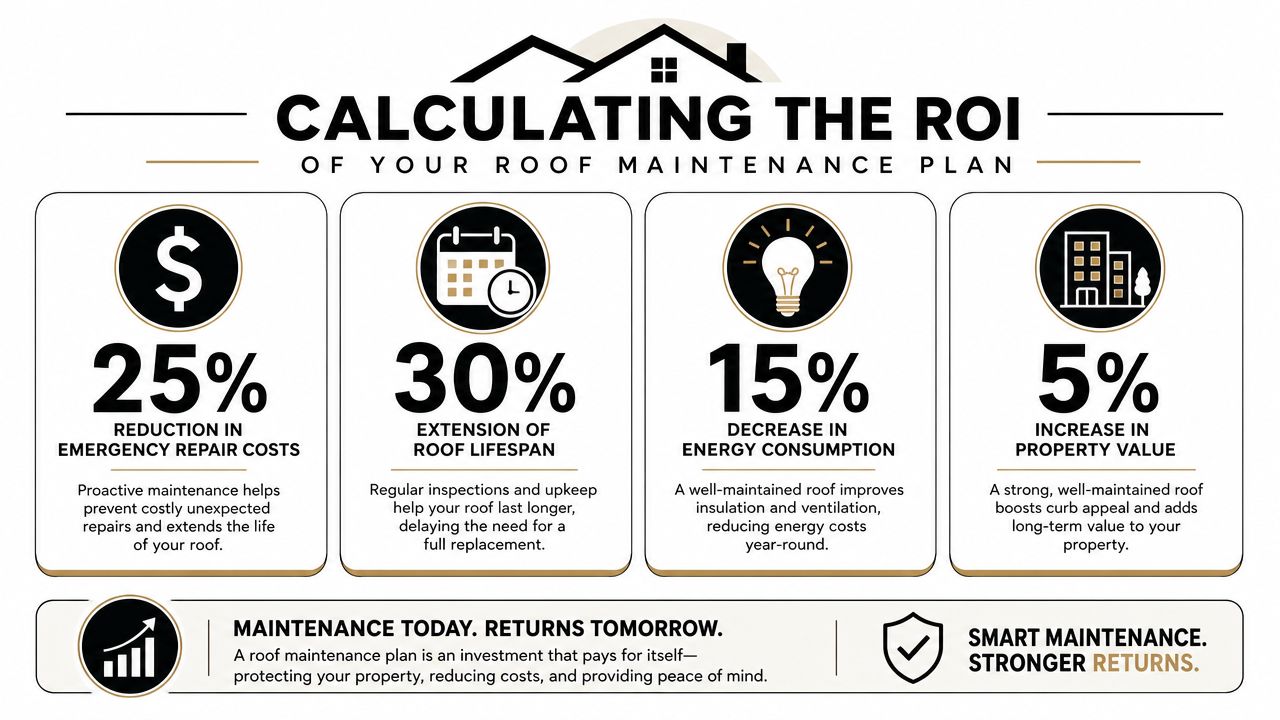

Calculating the ROI of Your Maintenance Plan

In South Florida, roof maintenance pays for itself the first time it prevents a leak during a storm, supports an insurance file after a hurricane, or buys you a few more years before a seven-figure replacement project hits the capital budget.

Replacement timing drives the real return

The biggest return usually does not come from one avoided repair invoice. It comes from delaying replacement while keeping the roof dry, insurable, and serviceable.

For a commercial property manager, that changes the math. A maintenance plan that helps a roof reach the upper end of its service life can defer a major capital expense for years. On a large South Florida building, that can mean more time to line up reserves, avoid disruptive work during peak occupancy, and plan around hurricane season instead of reacting to it.

The same roof defect also costs very different amounts depending on when it is found. A failed seal at a curb or penetration might be a small repair during a scheduled visit. After months of wind-driven rain, it can turn into wet insulation, interior damage, tenant complaints, and a much larger scope.

Emergency spending is expensive for a reason

Emergency roof work costs more because every part of the situation is working against you. The leak is active. Access is rushed. Materials and labor are being mobilized under pressure. The property team is trying to protect occupied space while making decisions with limited time and incomplete information.

That is bad asset management and bad budgeting.

The National Roofing Contractors Association has long recommended regular inspections and maintenance because roof systems perform better when defects are found and corrected early, as outlined in its commercial roof maintenance guidance. That lines up with what contractors see in the field. Roofs that get checked on schedule usually need smaller repairs, fewer emergency calls, and less interior remediation than roofs that are ignored until water shows up inside.

In South Florida, this matters even more. Hurricane exposure, UV intensity, ponding after heavy rain, and constant rooftop mechanical traffic all shorten the distance between a minor defect and a costly failure.

ROI includes insurance and documentation, not just repair savings

A lot of owners calculate return too narrowly. They compare annual maintenance fees to last year's repair spend and miss the larger financial pressure on the property.

Insurers want condition, history, and proof that the building is being managed responsibly. After a named storm, organized inspection reports and dated photos can help establish pre-loss condition and support a cleaner claim conversation. If records are missing, the owner has fewer advantages and more room for dispute.

Code pressure is part of the return too. In Florida, once roof damage crosses certain thresholds, repair work can trigger broader code requirements. Catching defects early helps keep work in the repair category instead of letting deterioration spread into a larger and more expensive project.

A practical way to evaluate return

Use a simple property-level comparison:

- Annual maintenance cost: predictable, budgeted, documented

- Emergency leak response: higher labor cost, tenant disruption, and short decision windows

- Interior damage risk: ceiling tile, flooring, drywall, inventory, and downtime

- Replacement timing: whether capital spending happens on your schedule or the roof's schedule

- Insurance and claim support: whether you have records that hold up after a storm

That is the true ROI calculation.

A maintenance plan protects the roof membrane, but it also protects cash flow, tenant stability, and decision-making. On South Florida commercial properties, where weather, insurers, and code enforcement all raise the stakes, that return is easy to underestimate until the roof is under stress.

Understanding the Costs of a Commercial Roof Plan

South Florida owners usually pay far more for deferred roof care than for scheduled roof care.

Maintenance pricing is driven by labor, roof complexity, and the amount of risk the contractor is being asked to manage. A clean, accessible low-slope roof with few penetrations costs less to service than a roof packed with HVAC curbs, conduit, satellite mounts, edge metal repairs, and recurring drainage issues. The difference is not markup games. It is time on the roof, number of leak-prone details, and the level of documentation needed to protect the property file.

For budgeting purposes, many commercial plans are priced on a per-square-foot, per-visit basis. On a 20,000-square-foot building, two scheduled service visits per year often land in the low-thousands annually, then move up if the roof needs corrective work, storm follow-ups, or extra reporting for ownership, warranty, or insurance files. That range is still small compared with one interior leak event in a medical office, retail center, or occupied warehouse.

What actually changes the price

Property managers should compare scope before comparing totals. The same square footage can produce very different proposals.

- Roof layout: More transitions, parapet walls, corners, and equipment curbs create more inspection and repair points.

- Roof system: TPO, modified bitumen, BUR, PVC, and metal all age differently and require different repair methods.

- Current condition: A neglected roof usually needs cleanup and corrective service before it settles into a normal cycle.

- Access: Limited ladder points, restricted parking, and tight roof hatches add labor time.

- Drainage and penetrations: Drains, scuppers, pipes, stands, and rooftop units are common leak locations and need close review.

South Florida adds another pricing factor. Hurricane season changes how contractors build these plans. Many owners want pre-storm inspections, post-storm condition checks, photo logs, and repair tracking that can support future claim discussions. That paperwork takes time, but it has value when a carrier asks what the roof looked like before the event.

What should be included in the scope

A real maintenance plan should spell out what the crew will do on the roof, what gets documented, and what happens when they find a defect. If the proposal is vague, the price is hard to trust.

A solid scope usually includes two scheduled inspections per year, drain and gutter cleaning, debris removal, sealant and flashing review, condition photos, and written recommendations for repairs. Branded reporting also matters. A clear roof inspection report sample and service documentation makes it easier for managers to show owners what was found, what was corrected, and what still needs budget approval.

{kind=link}

A quick screen helps:

| Proposal feature | Why it matters |

|---|---|

| Twice-yearly inspections | Creates a predictable review cycle before small defects spread |

| Drain and gutter cleaning | Reduces standing water and overflow risk |

| Debris removal | Lowers wear at drains, seams, and edge details |

| Photo reporting | Supports owner updates, warranty files, and storm records |

| Repair recommendations | Turns observations into a work list with priorities |

Low-cost plans usually cut one of two corners. They skip documentation, or they reduce the inspection to a basic walk-through with little technical review. Neither one gives a South Florida owner much protection.

Price should also be weighed against contractor qualifications. If roof access, jobsite control, and liability handling are weak, the cheap number can become expensive fast. This is one reason property teams should review the basics of hiring safely with bonded and insured before signing a service agreement.

In this market, the right question is not whether the plan is cheap. The right question is whether the plan is detailed enough to protect the building, support the file, and help the owner avoid a larger capital hit before the roof is ready for replacement.

Selecting a Roofing Partner for South Florida Properties

The right contractor for a South Florida maintenance program isn't just someone who can patch a leak. You want a partner who understands why this market forces higher standards.

Local climate knowledge changes the quality of the plan

South Florida roofs take punishment from UV exposure, humidity, wind-driven rain, and hurricane-season stress. The provider you hire should know how these conditions affect low-slope membranes, metal edge details, rooftop equipment curbs, sealants, and drainage layouts across Broward, Miami-Dade, and Palm Beach counties.

That local knowledge affects scheduling too. Inspections should align with the periods when weather shifts expose weak points fastest. Post-storm follow-up matters here in a way it may not in milder regions. A contractor who treats South Florida like any other market will miss things a local operator checks almost automatically.

Paperwork and protection are not administrative details

A quality maintenance plan requires formal record-keeping, including inspection reports, photos, and repair logs, and that documentation is commonly cited as important for warranty validation and storm-related insurance support, according to commercial roof maintenance record-keeping guidance.

That means your roofing partner should be able to produce organized records without being chased for them. If a building changes ownership, submits a claim, or reviews capital needs, those files become part of the asset history.

Licensing and insurance also matter for more than compliance. They're part of risk control. Property managers who want a simple outside explanation of hiring safely with bonded and insured can use that framework when vetting any vendor who sends crews onto occupied commercial property.

A provider's professional identity should be easy to verify too. Even something as basic as a recognizable roofing company brand mark signals whether the business operates like an established company or a phone number with a pickup truck.

South Florida property managers don't just need a roofer. They need records, responsiveness, and local judgment under storm pressure.

Questions worth asking before you sign

Don't rely on broad promises. Ask direct questions.

- Inspection process: What exactly gets checked on each visit?

- Documentation standard: Will you receive photos, locations, dates, and repair notes every time?

- Storm response: How are post-storm assessments handled?

- Repair workflow: Which minor issues can be corrected quickly, and which trigger separate approval?

- Roof traffic control: How do you protect the membrane when other trades access the roof?

The right answers are usually concrete, not polished. Good contractors talk about drains, curbs, penetrations, edge metal, membrane condition, reporting, and follow-up. Weak ones talk mostly about “keeping an eye on things.”

South Florida ownership comes with enough uncertainty already. Your roof plan should reduce it.

If you manage or own property in Broward, Miami-Dade, or Palm Beach County, Paletz Roofing and Inspections brings over 30 years of South Florida roofing experience, along with the inspection, repair, and documentation discipline a serious maintenance program requires. If you want a commercial roof maintenance plan built around storm exposure, warranty protection, and long-term asset preservation, contact their team for a detailed evaluation.