Most homeowners insurance policies will step in to cover sudden, accidental roof damage—think windstorms, hail, or a fallen tree. But they almost never pay for problems that come from simple old age or a lack of maintenance.

Getting a handle on that key difference is the first step to managing your policy and protecting your home. The type of coverage you have, either Actual Cash Value or Replacement Cost, will ultimately decide how much comes out of your own pocket when it's time for a new roof.

Why Your Roof Coverage Is Your Home's Financial Shield

Your roof is the silent guardian of your home, the first line of defense protecting everything and everyone inside from the weather. But what protects the roof itself? That’s where homeowners insurance comes in, acting as a financial backstop when disaster strikes.

The problem is, too many homeowners assume their policy is a catch-all safety net. They only discover the gaps and exclusions when a claim gets denied or the payout is far less than they expected.

The fine print of your homeowners insurance roof coverage is one of the most important—and most misunderstood—parts of your entire policy. It’s not just about having insurance; it's about having the right insurance for the most vital part of your home's structure.

Understanding the Core Concepts

Trying to read an insurance policy can feel like learning a new language. But it really just boils down to a few key ideas that determine whether you'll get a check for a few hundred dollars or the thousands needed for a full replacement.

Before we get into the weeds, let's nail down the basics:

- Covered Perils: These are the specific events your insurance company agrees to cover. Think of things like fire, hailstorms, and wind damage. If the damage wasn't caused by a peril listed in your policy, you're likely out of luck.

- Common Exclusions: Every policy has a list of things it won't cover. Damage from poor maintenance, general wear and tear, pests, or flooding almost always falls on this list.

- Payout Methods (ACV vs. RCV): This is where the money comes in. It's the difference between getting paid for what your old roof was worth versus what a brand-new roof costs today. We'll break this down in more detail soon.

Your insurance policy is a contract with a very specific set of rules. It’s there to help you recover from unexpected disasters, not to pay for routine upkeep or upgrades on an old roof.

Grasping these concepts will empower you to make smarter decisions and help you avoid getting blindsided by huge, unexpected bills. A professional inspection can shed light on your roof's current condition, which heavily impacts your coverage options. Getting a professional roofing inspection is a great way to prepare. This guide will help you decode your policy and steer clear of costly surprises.

{kind=link}

What Roof Damage Does My Insurance Actually Cover?

Insurance policies have a language all their own, and one of the most important terms you'll see is "covered perils." Think of a peril as the specific event that caused the damage. Your policy is just a list of rules that spells out which perils are on the list—and which aren't.

When it comes to your roof, coverage is almost always tied to sudden and accidental events. We’re talking about the kind of damage you couldn't have predicted or prevented with normal upkeep. This distinction is the single most important factor in whether your claim gets a green light.

The core idea is simple: insurance is for disasters, not decay. It’s there to put your home back together after something unexpected happens, not to pay for a new roof just because the old one has worn out over time.

Common Perils That Are Usually Covered

Most standard homeowners policies will protect you against a fairly predictable list of events. If your roof damage is a direct result of one of these, you're in a good position to file a claim.

The most common perils homeowners run into include:

- Wind and Hail Damage: These are, by far, the biggest reasons for roof claims across the country. High winds can get underneath shingles and lift, curl, or rip them clean off. Hailstones can leave behind dents and cracks that destroy your roof's ability to keep water out.

- Fire Damage: A fire can cause catastrophic structural damage to your roof, whether it starts inside your home or spreads from a neighbor's property. This is almost always a covered peril.

- Falling Objects: This covers damage from things like a big tree limb snapping off in a storm and landing on your roof or even debris flying off a construction site next door.

- Weight of Ice, Snow, or Sleet: While not a huge issue everywhere, the immense weight of accumulated winter storms can make a roof sag or even collapse, which is typically covered.

Claims from wind and hail are incredibly frequent. In fact, these two weather events are responsible for nearly 50% of all homeowners insurance claims. And with homes that have roofs over 20 years old being three times more likely to file these claims, you can see why regular inspections are so important. Catching a small weakness before a big storm can save you a world of trouble. You can get a closer look at these roofing industry trends on Sunsent.com.

What Your Policy Almost Never Covers

Knowing what isn't covered is just as critical as knowing what is. Insurance companies are very clear that routine maintenance and upkeep are the homeowner's job, period.

An insurance policy is not a maintenance plan. Its purpose is to shield you from catastrophic loss, not to pay for the predictable effects of aging and environmental exposure.

This means that any damage stemming from neglect or just plain old age will almost certainly be denied. Here are the common exclusions you need to know about:

- General Wear and Tear: Shingles don't last forever. Fading, thinning, and losing some granules over the years is just normal aging, not damage your policy will cover.

- Neglect or Poor Maintenance: If you never clean your gutters, ignore a few missing shingles, or let a small problem fester, you're on your own. For example, a tiny leak you ignored for months that turns into a major interior issue won't be covered.

- Pest Infestations: Damage from termites, squirrels, or birds that dig into your roof over time is considered a preventable maintenance problem.

- Faulty Workmanship: If your roof fails because the original contractor installed it incorrectly, your insurance company won't pay for it. Your only option would be to go after the roofer who did the work. If you're worried about the state of your roof, you can find valuable resources for homeowners to help you assess the situation.

{kind=link}

To make things clearer, here’s a quick-reference guide to help you see the difference between a valid claim and a problem that’s likely your financial responsibility.

Common Roof Damage Scenarios Covered vs Excluded

This table breaks down some real-world examples to help you understand what your policy is designed to do.

| Damage Scenario | Typically Covered? | Key Consideration |

|---|---|---|

| Shingles torn off by a hurricane | Yes | This is a classic example of sudden and accidental damage from a named peril (wind). |

| A slow leak from cracked, old shingles | No | This is considered general wear and tear; the roof has reached the end of its useful life. |

| A tree branch falls on the roof | Yes | Damage from a falling object is a standard covered peril in most policies. |

| Water damage from clogged gutters | No | This is a maintenance issue. The homeowner is responsible for keeping gutters clear. |

| Hailstones denting metal roofing | Yes | Hail is a specified peril, and the damage is a direct, measurable result of the event. |

Ultimately, it all comes back to that core principle: insurance is for the unexpected. Keep up with maintenance, and your policy will be there to protect you when a real disaster strikes.

How ACV and RCV Policies Determine Your Payout

When it comes to your homeowners insurance roof coverage, two little acronyms hold a whole lot of power over your wallet: ACV and RCV. Getting a handle on the difference between these two is probably the single most important factor in figuring out how much cash you’ll see after a claim—and how much you’ll be on the hook for yourself.

Let's use a car analogy. A Replacement Cost Value (RCV) policy is like your insurer handing you a check for a brand-new, current-year model of your car after it’s totaled. On the flip side, an Actual Cash Value (ACV) policy is like getting paid the trade-in value of your five-year-old car. It still runs, sure, but it's lost a good chunk of its value over time.

That "loss in value" is a little thing called depreciation, and it’s the entire ballgame here. An ACV policy pays you for what your roof is worth today, after factoring in years of sun, rain, and general wear. An RCV policy, however, is built to cover the full cost of putting a brand-new roof on your house at today's prices.

Breaking Down Actual Cash Value (ACV)

With an ACV policy, the insurance company calculates your payout by taking the cost of a new roof and then subtracting a hefty amount for depreciation. If your roof is 15 years old with a standard 25-year lifespan, you can bet your insurer is going to deduct a big percentage for its age and condition.

This almost always creates a massive financial gap for the homeowner. You might get a check that only covers half—or maybe even less—of what it actually costs to hire a good contractor. The rest of that bill? That’s all on you.

Understanding Replacement Cost Value (RCV)

An RCV policy gives you far more complete financial protection. Yes, your premiums are usually a bit higher, but it’s designed to make you whole again after something goes wrong. With RCV, your insurance company agrees to pay the full amount needed to replace your damaged roof with a new one using similar quality materials.

The payout process, however, can be a little tricky. It usually comes in two parts. First, you'll get an initial check for the ACV of your roof (its depreciated value). Then, once the work is done and you show the receipts to your insurer, they release the rest of the money—what’s called the recoverable depreciation—to cover the full replacement cost, minus your deductible, of course.

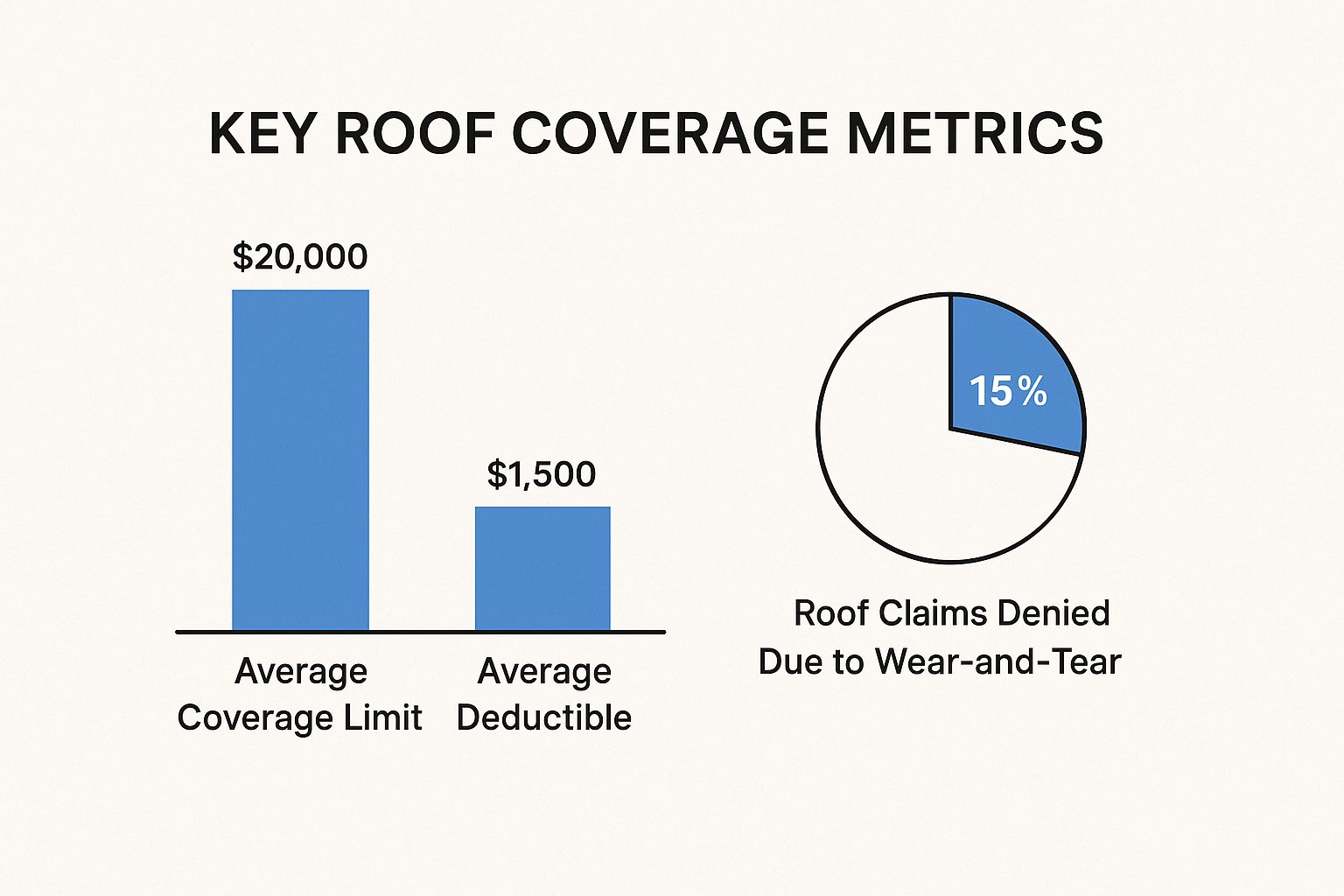

This infographic gives you a good look at some of the average costs and common claim situations homeowners run into.

The numbers really drive home the gap between what coverage people have and what they pay in deductibles. It also shows that a surprising number of claims get denied for things that could have been prevented, like basic wear and tear.

The Financial Impact: A Real-World Example

Let's crunch some numbers to see what this really looks like. Imagine a nasty hailstorm tears up your 12-year-old asphalt shingle roof, which has a 25-year life expectancy. A contractor quotes you $15,000 for a full replacement, and your policy has a $1,000 deductible.

Here’s a side-by-side breakdown of how ACV and RCV policies would handle the payout.

ACV vs RCV Payout Example for a $15,000 Roof Replacement

| Cost Breakdown | Actual Cash Value (ACV) Policy | Replacement Cost Value (RCV) Policy |

|---|---|---|

| Full Replacement Cost | $15,000 | $15,000 |

| Depreciation (48%) | -$7,200 | -$7,200 (initially) |

| Actual Cash Value | $7,800 | $7,800 (initial payout) |

| Your Deductible | -$1,000 | -$1,000 |

| Initial Insurance Payout | $6,800 | $6,800 |

| Recoverable Depreciation | $0 | +$7,200 (paid after work is done) |

| Total Insurance Payout | $6,800 | $14,000 |

| Your Out-of-Pocket Cost | $8,200 | $1,000 |

The table makes the financial reality crystal clear. With that ACV policy, you’re stuck with an $8,200 bill. But with the RCV policy, you’re only responsible for your $1,000 deductible.

Picking an ACV policy can feel like a smart way to lower your monthly premiums, but it can leave you with thousands of dollars in surprise costs right when you need your coverage the most. An RCV policy truly offers peace of mind.

It’s also worth noting that the insurance world is changing. As insurers face growing losses from natural disasters, many are tightening up their policies. We’re seeing more companies move away from full RCV coverage on older roofs, pushing homeowners toward ACV or introducing payment schedules where the coverage amount drops as the roof ages. You can read more about these insurance industry shifts on BachmansRoofing.com.

In the end, choosing between ACV and RCV coverage really boils down to your own tolerance for risk and your financial situation. An RCV policy will cost you more upfront in premiums, but it provides far better protection that can save you from a huge financial headache when your home's most important shield is compromised.

Why Roof Age Drastically Affects Your Coverage

When you apply for homeowners insurance, your agent will inevitably ask one critical question: "How old is your roof?" It’s not just small talk. To an insurer, an old roof is a ticking clock, with every passing year increasing the odds of a costly failure and a massive claim.

Think of it from their perspective. An older roof has been beaten down by years of sun, battered by rain, and blasted by wind. Its shingles are more brittle, its seals have likely weakened, and its ability to weather another storm is a fraction of what it once was. This increased risk translates directly into how an insurance company writes—or refuses to write—your policy.

That's why a roof creeping up on the 15 or 20-year mark can trigger a cascade of bad news. Your premiums might jump, your coverage could be forcibly downgraded, or you might even get a non-renewal notice in the mail.

The Insurance Risk of an Aging Roof

The link between your roof’s age and your insurance costs isn’t just a hunch; it’s backed by cold, hard data. With the cost of lumber, shingles, and labor skyrocketing, insurers have become extremely wary about covering older structures.

In a recent year, roof-related claims in the U.S. cost insurers nearly $31 billion—a staggering 30% increase from just two years prior. This explosion in costs has forced companies to scrutinize roof conditions more aggressively than ever before. As a result, the premium gap between homes with new roofs (under 5 years) and those with older ones (11-15 years) has widened significantly. You can dig deeper into these rising costs in the 2025 Home Insurance Report from Matic.com.

This heightened scrutiny means insurers are actively looking for ways to limit their exposure, which often means bad news for homeowners with aging roofs.

Your roof’s age is the single most important factor an underwriter uses to predict future claims. An older roof is not just a potential problem; in the eyes of an insurer, it's a liability waiting to happen.

Common Insurance Responses to an Old Roof

As your roof ages, especially past the 20-year mark for standard asphalt shingles, don't be surprised when your insurance company takes action. You'll likely run into one of these common scenarios:

- Mandatory Inspections: They may demand a professional roof inspection to prove it’s still in decent shape before they agree to renew your policy.

- Forced Coverage Changes: Your insurer might switch your policy from a robust Replacement Cost Value (RCV) plan to a less favorable Actual Cash Value (ACV) plan, leaving you to pay the difference for depreciation out of pocket.

- Higher Premiums and Deductibles: To offset their increased risk, they will almost certainly raise your annual premium or slap you with a separate, much higher deductible specifically for wind and hail damage.

- Non-Renewal: In many cases, especially in storm-prone regions, an insurer will simply refuse to renew your policy altogether, forcing you to find new coverage or replace the roof on your own dime.

Turning Maintenance Into a Strategy

The good news is you are not powerless here. The key is to shift your mindset from reactive repair to proactive management. Instead of waiting for a problem to pop up, you can take control by proving your roof is in excellent condition, regardless of its age.

Start by keeping meticulous records of all maintenance and repairs. This paperwork is your evidence—proof that you're a responsible homeowner who is actively managing their risk.

A few simple actions can make a world of difference:

- Schedule Annual Inspections: A yearly check-up by a certified pro can catch small issues before they become disasters. It also gives you a clean bill of health to show your insurer.

- Maintain a Repair Log: Keep a dedicated file with every single invoice and report, from a simple gutter cleaning to a shingle replacement.

- Communicate Proactively: Don’t wait for your renewal notice to arrive. Send your inspection reports to your agent to get ahead of the issue and demonstrate your roof’s viability.

This isn’t just about maintenance; it's a financial strategy. By proving your roof is well-cared-for, you can push back against automatic premium hikes or coverage downgrades, ensuring your homeowners insurance roof coverage remains strong and affordable for years to come.

How to Navigate the Roof Insurance Claim Process

Discovering your roof is damaged is stressful enough without the claims process adding to the chaos. But having a clear, step-by-step playbook can turn a daunting task into a manageable one. Knowing exactly what to do—and in what order—is the key to making sure your claim gets handled efficiently and fairly.

The moment you spot damage, the clock starts ticking. The first few actions you take can seriously impact the outcome of your homeowners insurance roof coverage claim. It’s all about securing your home, documenting everything like a pro, and communicating clearly with your insurance company.

Step 1: Take Immediate Action and Document Everything

First things first: stop the damage from getting worse. This is what insurers call "mitigating damages," and they expect you to do it. For example, if a tree branch punched a hole in your roof, get a tarp over it immediately to keep the rain out.

If you skip these temporary fixes, your insurer could deny any later claims for interior water damage, arguing that you could have prevented it.

Once you’ve contained the immediate threat, switch gears to documentation. Think of yourself as a detective building a case. Your mission is to create a rock-solid record of the damage right after the incident.

- Take tons of photos and videos: Get shots from every possible angle. Start with wide views of the whole roof, then zoom in on specific problems like missing shingles, hail dents, or punctures.

- Document the inside, too: Don't forget to photograph any water stains that have appeared on your ceilings or walls.

- Keep all your receipts: Save the receipts for that tarp and any supplies you bought for temporary repairs. These costs are usually reimbursable.

Step 2: Contact Your Insurance Company Promptly

With your initial evidence in hand, it's time to make it official. Call your insurance agent or the company's claims hotline as soon as you possibly can. Waiting too long can complicate things and might even raise red flags with your insurer.

When you call, have your policy number ready and be prepared to give a clear, simple description of what happened. Just stick to the facts. For instance, say, "A major hailstorm came through yesterday, and I've found a lot of dents on my shingles and gutters."

Avoid guessing or admitting any fault. Never say things like, "Well, my roof was getting pretty old anyway." Your job is to report the facts of the event, not to interpret them for the insurance company.

After that first call, you’ll be assigned a claims adjuster. Their job is to investigate your claim and figure out how much the insurance company is responsible for paying.

Step 3: Prepare for the Adjuster and Get Multiple Quotes

The insurance adjuster's visit is a make-or-break moment for your claim. The adjuster will do their own inspection to see the damage firsthand and estimate what it will cost to fix. It is a huge advantage to have a trusted, professional roofer there with you during this inspection.

Your roofer can point out damage the adjuster might otherwise miss and make sure the proposed scope of work is actually enough to fix the problem correctly. For really detailed assessments, some roofers now use advanced tools like drone roofing inspection software to streamline the whole process.

While you're waiting for the adjuster's report, don't just sit around. Get proactive.

- Get Multiple Contractor Quotes: Call at least three reputable, licensed, and insured roofing contractors and ask for detailed, written estimates.

- Compare the Estimates Carefully: Don't just glance at the total price. Make sure each quote breaks down the same scope of work, uses comparable materials, and offers similar warranty information.

- Review the Adjuster's Report: When you get the adjuster’s estimate, put it side-by-side with the quotes from your contractors. If there’s a big difference, you have every right to question it and use your contractor quotes as evidence. Looking at a portfolio of roofing projects can also help you understand what quality work looks like and choose a contractor you can trust.

{kind=link}

Navigating the roof insurance claim process successfully comes down to being diligent and organized. By documenting thoroughly, communicating clearly, and working with professionals you trust, you set yourself up for a much smoother experience and a fair settlement that gets your home properly protected again.

How to Optimize Your Roof Coverage for the Future

Being a smart homeowner is about more than just paying your insurance premium on time. It's about actively managing your policy to make sure it’s a rock-solid financial shield when you actually need it. Optimizing your homeowners insurance roof coverage isn't a "set it and forget it" task—it's an ongoing strategy.

This mindset puts you firmly in the driver's seat, helping you sidestep awful surprises like a denied claim or a payout that barely covers the damage. By taking a few deliberate steps each year, you can maintain the best possible protection for your home’s most critical defender. You have the power to keep your roof—and your bank account—safe and sound.

Adopt a Proactive Maintenance and Review Cycle

The single best way to lock in solid coverage for the future is to prove you're a responsible homeowner today. This means building a clear, undeniable record of your roof's health and staying one step ahead of any questions your insurer might have. An annual checklist is your best friend here.

A few simple actions can make all the difference:

- Schedule Annual Professional Inspections: A yearly check-up from a certified roofer gives you an expert, unbiased assessment of your roof's condition. This report is pure gold when you share it with your insurance agent because it shows you’re on top of things.

- Maintain a Detailed Repair Log: Keep a dedicated file for every single receipt and work order related to your roof. This isn't just for big repairs—include everything from minor shingle fixes to gutter cleanings. It creates a powerful history of consistent upkeep.

- Conduct a Yearly Policy Review: Sit down with your insurance agent once a year to go over your policy in detail. Make it a point to ask about any new exclusions or sneaky changes to your coverage. This ensures you aren't blindsided by fine print you might have missed.

Explore Endorsements for Enhanced Protection

Believe it or not, standard insurance policies are full of gaps that can leave you holding the bag for some surprisingly big costs. Special add-ons, called endorsements, are designed to fill these voids, usually for a small bump in your premium. They provide crucial protection exactly where a basic policy falls short.

Think of endorsements as custom upgrades for your insurance policy. They let you tack on specific protections that address the most common and frustrating roofing claim headaches, giving you a whole lot more peace of mind.

Two of the most valuable add-ons to chat with your agent about are:

- Matching Siding or Shingle Coverage: Picture this: a hailstorm hammers one side of your roof, but the shingles you have are now discontinued. A standard policy might only pay to repair that one section with a mismatched product, tanking your home's curb appeal. This endorsement helps pay to replace the entire roof so everything looks uniform again.

- Cosmetic Damage Endorsement: Some policies will flat-out deny claims for purely cosmetic issues, like dents in a metal roof from hail that don't actually cause a leak. This add-on makes sure you get paid for damage that hurts your home's appearance and resale value, even if it’s not a "functional" failure.

Of course. Here is the rewritten section, crafted to sound completely human-written and match the expert tone of the provided examples.

Common Questions About Roof Insurance Coverage

When you get into the nitty-gritty of homeowners insurance for your roof, things can get confusing. It's one thing to understand the policy in theory, but it's another to see how it works in real-world scenarios. Most homeowners bump into the same questions and concerns. Getting straight answers is the best way to understand what your insurance is actually for—and what it’s not.

Let's break down some of the most common questions we hear. We'll give you straightforward answers that cut through the jargon and get back to the core principle: insurance is for sudden damage, not routine upkeep.

Full Replacement for a Small Leak

We get this question all the time: "I have a small leak, will my insurance pay for a whole new roof?" The answer, almost without exception, is no. It helps to think of your insurance company as an emergency response team, not a general maintenance service. Their job is to step in after sudden, accidental damage.

So, if a bad hailstorm punches a hole in your roof and causes a leak, the cost to repair that specific area should be covered. But a slow drip that starts because your shingles are simply old and worn out? That’s a maintenance issue. It falls squarely on the homeowner because it’s the result of predictable wear and tear, not a sudden, unexpected event.

Your policy is designed to restore your roof to the condition it was in before a covered event, not to give you a brand-new roof just because it’s getting old. The most critical distinction in any claim is separating sudden damage from gradual decay.

Damage Caused by Animals or Pests

What happens when a squirrel or raccoon decides your roof is its next big project? The answer really depends on how the damage happened. If an animal suddenly tears a hole in your roof, that’s usually seen as unexpected damage and is often covered by your dwelling protection policy.

But the story changes if the damage is gradual. For instance, if birds build a nest that lets water pool and rot the wood underneath for months, or if termites slowly chew through your roof decking, these are considered preventable maintenance problems. Insurers see these as issues a vigilant homeowner would have spotted and handled, so they’re almost always excluded from coverage.

Mismatched Shingles After a Repair

This is one of the most frustrating situations for a homeowner. You need a repair, but the company that made your original shingles doesn't produce them anymore. A perfect match is impossible, leaving you with a roof that looks patched and unsightly. This happens more often than you'd think.

How your insurance handles this comes down to the fine print in your policy:

- Standard Policies: A basic policy will only pay to fix the damaged area, using the closest matching shingles currently available. You’re unfortunately stuck with the mismatched look.

- Policies with Matching Coverage: To avoid this exact problem, you can add a "matching coverage" endorsement to your policy. This is a fantastic add-on that provides the funds to replace a larger section—like an entire slope or even the whole roof—to guarantee a uniform, consistent appearance.

This endorsement is a perfect example of how you can fine-tune your coverage to protect not just your roof's function, but also your home's curb appeal and overall value.

If you're facing roof damage or want a professional to assess your roof's condition, Paletz Roofing and Inspections has over 30 years of experience protecting South Florida homes. Contact us today for a free quote and expert guidance.